Institutional Capital Is Validating Home Equity as an Asset Class

There’s no question: Home Equity Investment (HEI) strategies are moving into the mainstream.

Over the past few months, several major institutional commitments have signaled growing confidence in this emerging category:

- Blue Owl Capital announced a $2.5 billion capital commitment in the home equity investment space, alongside an additional $2 billion commitment supporting reverse mortgage products.

- MidOcean Partners agreed to purchase up to $600 million of home equity investments, reinforcing institutional demand for housing-based asset strategies.

- And, of course, Cornerstone Financing secured up to a $1 billion financing commitment from Fortress Investment Group to expand the availability of CHEIFS across advisors and brokers.

Taken together, these commitments represent more than $6 billion of recent institutional capital flowing into home equity funding, signaling that this category is rapidly moving into the financial mainstream.

What the Recent Capital Commitments Are Really Saying

When institutional investors commit billions to a category, they are signaling confidence in three things: durability, scalability, and long-term relevance.

We are seeing home equity products evolve beyond emergency liquidity tools or consumer-first alternatives. Instead, capital markets are validating home equity as a flexible financial instrument that can support planning, income, longevity, and balance-sheet optimization.

This mirrors the evolution we’ve seen in other asset classes—where early consumer adoption is followed by institutional refinement and discipline.

Not All Home Equity Models Are the Same

As interest and investment increase, it’s critical to recognize that not all home equity solutions are created equal.

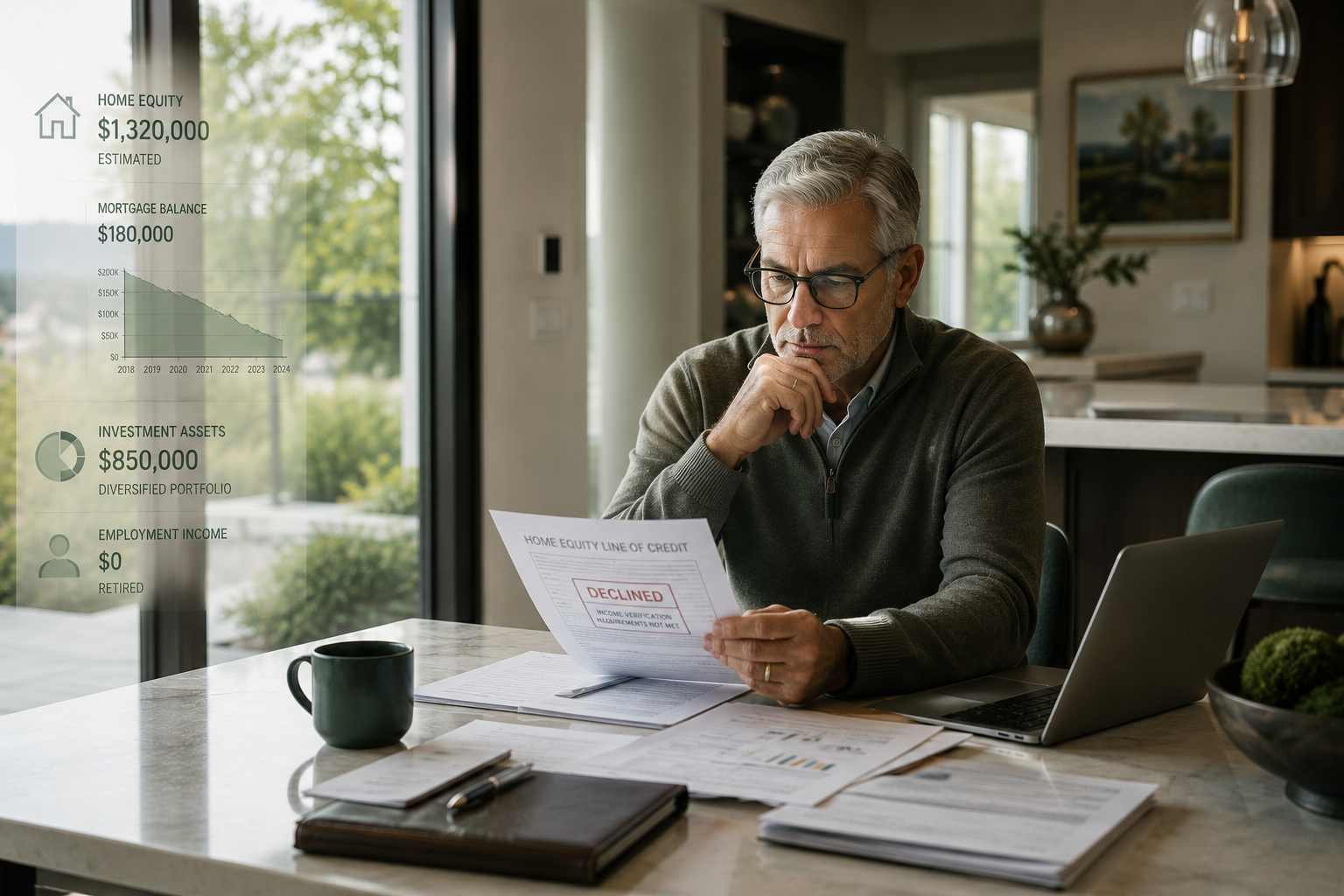

As the category grows, it’s important to recognize that not all HEI products are designed for the same purpose. Some are built for short-term consumer liquidity needs (with terms that reflect the weaker creditworthiness of the customer being served). In contrast, others are structured specifically for use within professional financial-planning environments, where suitability, transparency, and long-term alignment are critical.

That distinction becomes increasingly important as advisors, RIAs, and insurance professionals look to integrate home equity into holistic financial strategies rather than one-off decisions.

Why This Moment Matters for Advisors

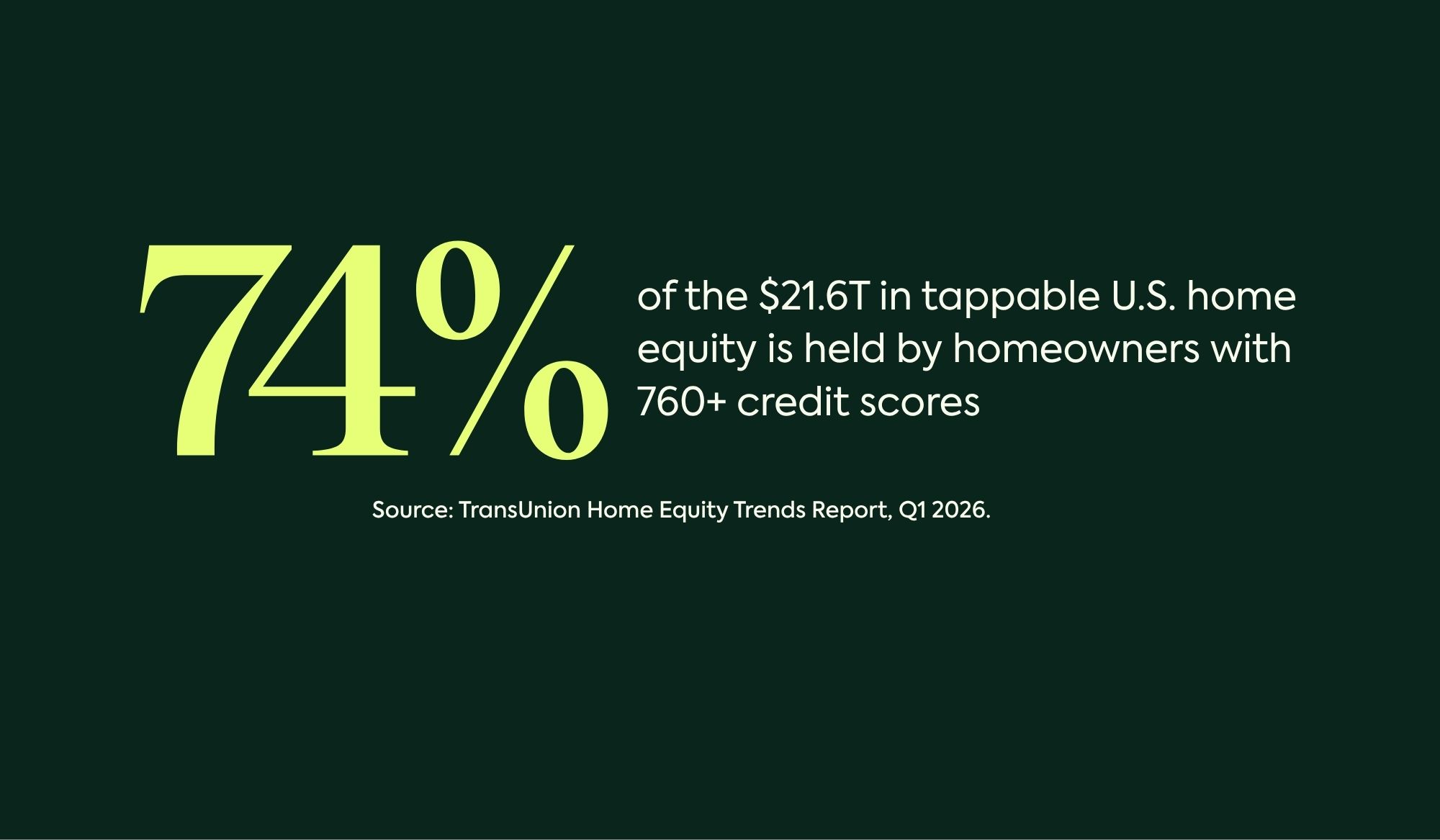

For mass-affluent homeowners, HEI solutions must be evaluated alongside other prime home-financing options, as well as against the use of liquidating cash and/or investment portfolios. These clients typically have strong credit profiles, significant home equity, and multiple choices available to them. Any HEI used in this context must compete on a lower-cost structure, transparency, and long-term outcomes, not urgency.

For financial professionals, this influx of institutional capital should prompt a deeper question:

How does home equity fit responsibly into a client’s broader financial picture?

Used correctly, home equity can help:

• Preserve portfolio assets during volatile markets

• Create liquidity without triggering forced asset sales

• Support retirement income strategies

• Enable insurance and legacy planning decisions

The conversation is shifting from access to *application*—and from novelty to normalization.

Our Perspective

At Cornerstone Financing, we’ve long believed that prime-oriented HEI products would emerge as a core financial-planning tool for mass-affluent homeowners, not a last-resort solution.

Our focus has never been on chasing headlines. It’s been on building infrastructure, governance, and partnerships that allow home equity to be used thoughtfully, transparently, and in alignment with long-term financial outcomes.

The recent wave of institutional investment reinforces what we’ve seen firsthand: home equity is moving into the core of modern financial planning. That belief is what led us to build CHEIFS as a planning-first, prime HEI designed to sit alongside traditional wealth, insurance, and mortgage strategies.

Looking Ahead

As the category continues to mature, the winners will not be defined by capital alone, but by clarity of purpose.

The future of home equity will be shaped by models that respect the complexity of homeowners’ financial lives and empower professionals to guide its use responsibly.

The capital is arriving. The question now is how wisely it will be deployed.

About the Author

Vincent Mazza is the Chief Marketing Officer of Cornerstone Financing, where he oversees brand strategy, product positioning, and go-to-market efforts for the company’s home equity solutions. With more than two decades of experience in digital strategy, financial services marketing, and advisor-focused growth initiatives, Vincent works closely with leadership, capital partners, and distribution teams to help position home equity as a responsible, planning-driven financial instrument.