Turning Home Equity Into a Retirement Planning Advantage

Link copied

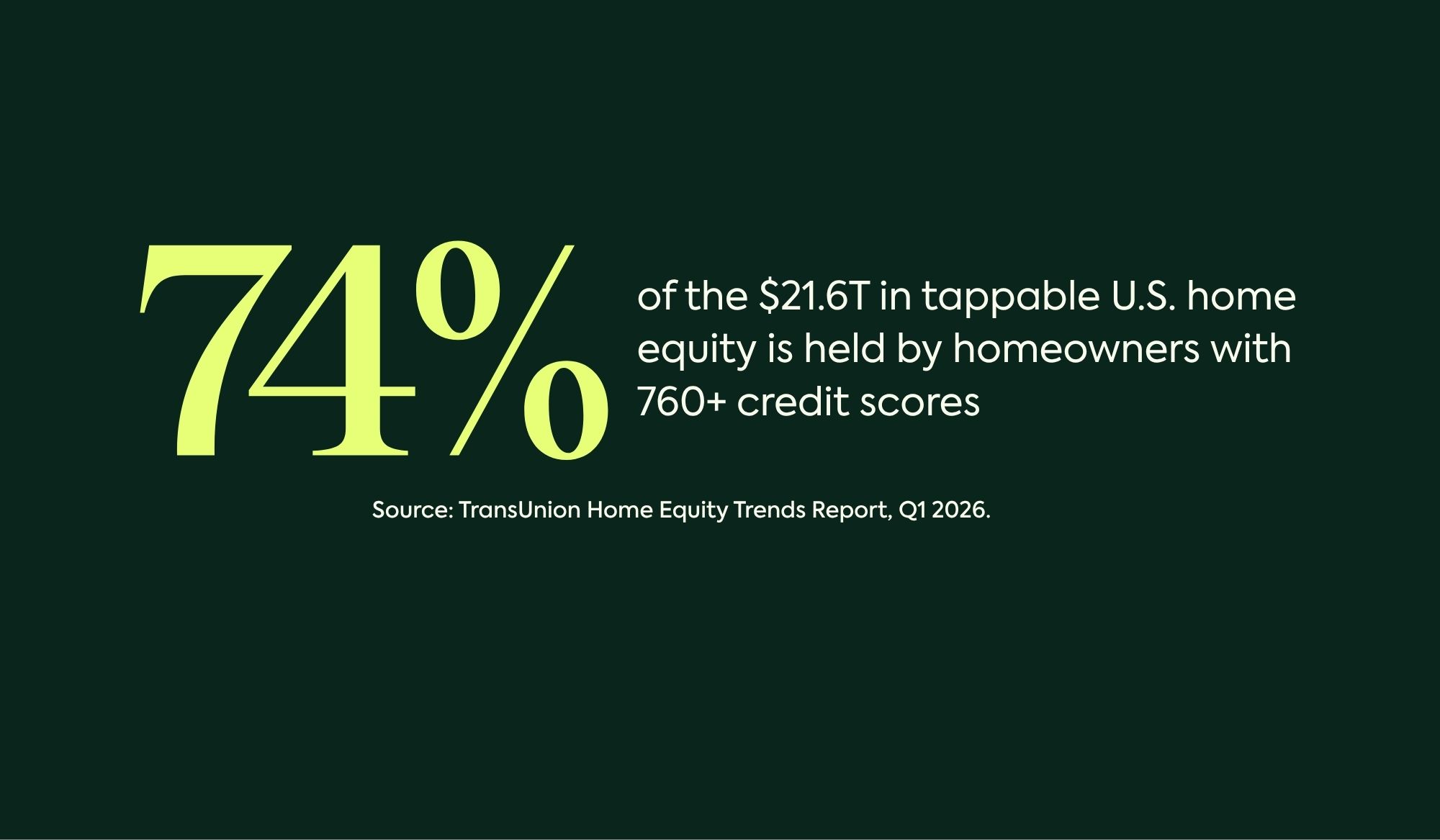

Home equity has quietly become one of the largest — and most underutilized — assets on the household balance sheet. As retirement planning grows more complex, advisors and homeowners alike are searching for smarter ways to create liquidity without disrupting long-term plans.

At Cornerstone Financing, we believe home equity should be treated as a strategic planning asset, not a last-resort funding source. Through CHEIFS®, homeowners can access a portion of their home equity without debt, monthly payments, or a required term — while retaining ownership and control of their home.

This approach opens the door to powerful planning use cases, including retirement income optimization, long-term care planning, and — most notably — tax-efficient Roth conversions.

In our upcoming podcast on 62WhoKnew, we explore how advisors are combining institutional capital, home equity, and modern planning software to help clients improve outcomes in a rising-tax environment.

Supercharging Roth Conversions with Home Equity

Roth conversions are one of the most effective tools available to manage future tax exposure. Yet many households hesitate to convert because of the upfront tax cost.

CHEIFS provides an alternative funding source — allowing homeowners to reposition a portion of their home equity to cover conversion taxes without liquidating investment assets or taking on debt.

- It preserves portfolio integrity

- It avoids required monthly payments

- It aligns with long-term planning rather than short-term borrowing

Most importantly, it is fully modelable within Wealthy and Wise+, allowing advisors to clearly illustrate before-and-after outcomes for clients.

Watch the full conversation on 62WhoKnew to see a real-world example of using home equity to fund Roth conversions without debt, payments, or a required term.