Designing Proactive Financial Strategies to Avoid Reactive Decisions

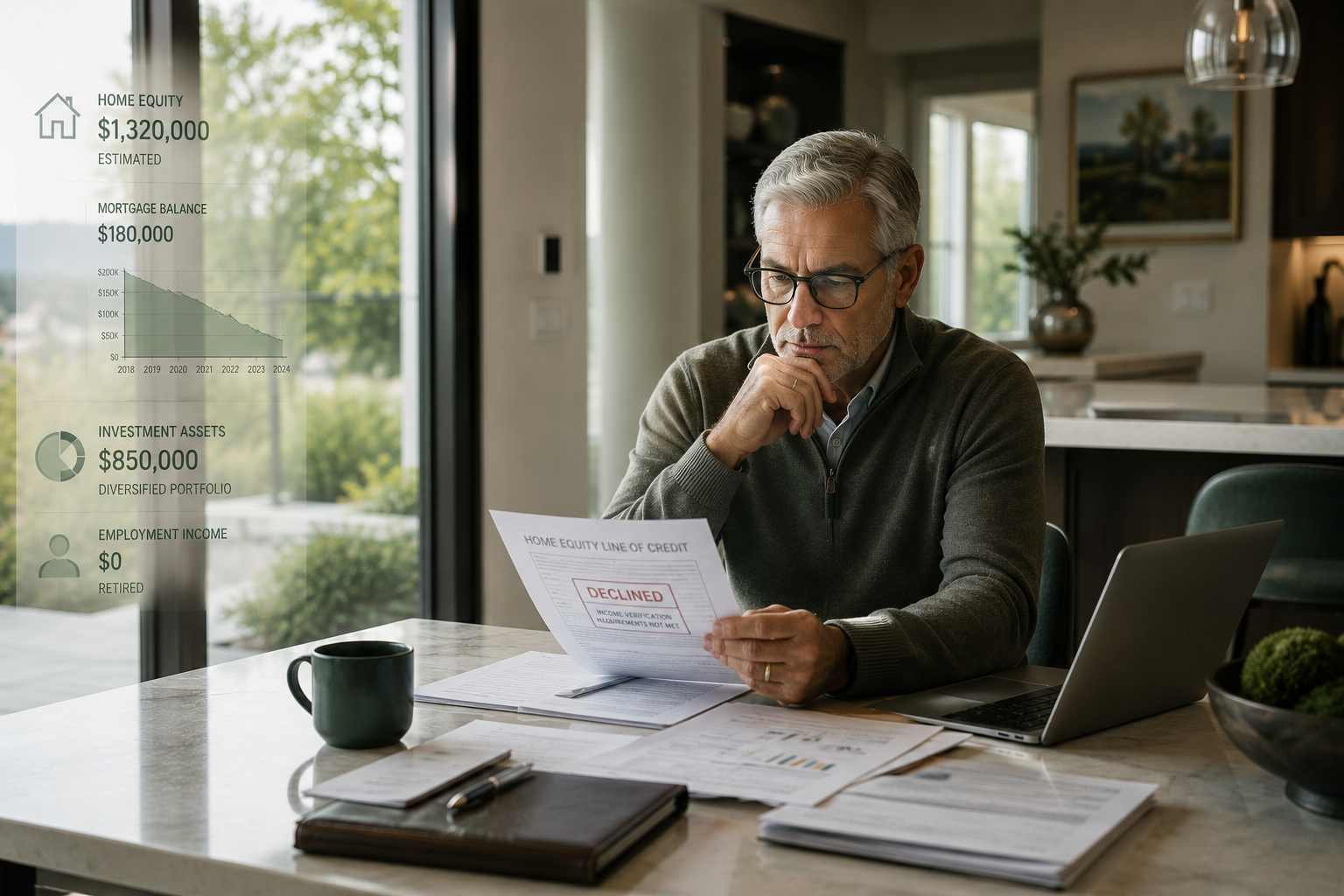

Recent reporting in The New York Times highlights a deeply human concern: aging parents and relatives making financial decisions that expose them to unnecessary risk, fraud, or long-term harm. The article focuses on what families can do once something already feels off — after a suspicious check, a questionable investment, or a confusing financial move.

But another important question often comes earlier: why do many financial decisions happen under such intense time pressures in the first place?

In many cases, it’s because key choices are being made only after options have narrowed — when stress is high and flexibility is limited. As the saying goes, “An ounce of prevention is worth a pound of cure.” Approaching financial planning earlier, before urgency sets in, can reduce pressure and expand the range of choices available.

This can be especially true with home equity.

Ask yourself this simple question: Does truly owning a $1 million home feel any differently if you have a $700,000 mortgage versus a $500,000 mortgage?

Your memories, sense of safety, and attachment to the home remain constant. For many, homeownership still feels familiar day to day.

But financially, many homeowners notice the difference between $500,000 of home equity and $300,000 — like how people may perceive the financial improvement a $100,000 gain makes in an investment portfolio, even before acting on it.

So, why is home equity often treated differently from other financial assets that can be allocated or repositioned? Many homeowners wait until late in the process to tap home equity, even though it could serve as a strategic resource.

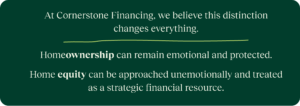

The difference often relates more to psychology than math. Homeownership is emotional and often prioritized in ways other financial assets are not. Home equity is a financial resource, and some homeowners consider ways it might be used strategically on the balance sheet.

As long as the approach to using home equity does not jeopardize homeownership, home equity can be viewed as a source of liquidity that may be accessed proactively to support sound financial planning.

The Foundation of CHEIFS®

This distinction is the foundation of how CHEIFS was designed.

It is why we work with professional insurance and financial advisors to bring CHEIFS to homeowners. It is why CHEIFS is integrated into planning platforms like Wealthy and Wise+™ by InsMark®. And it is why home equity can now be evaluated, modeled, and used like any other planning asset — without selling the home or taking on traditional debt financing.

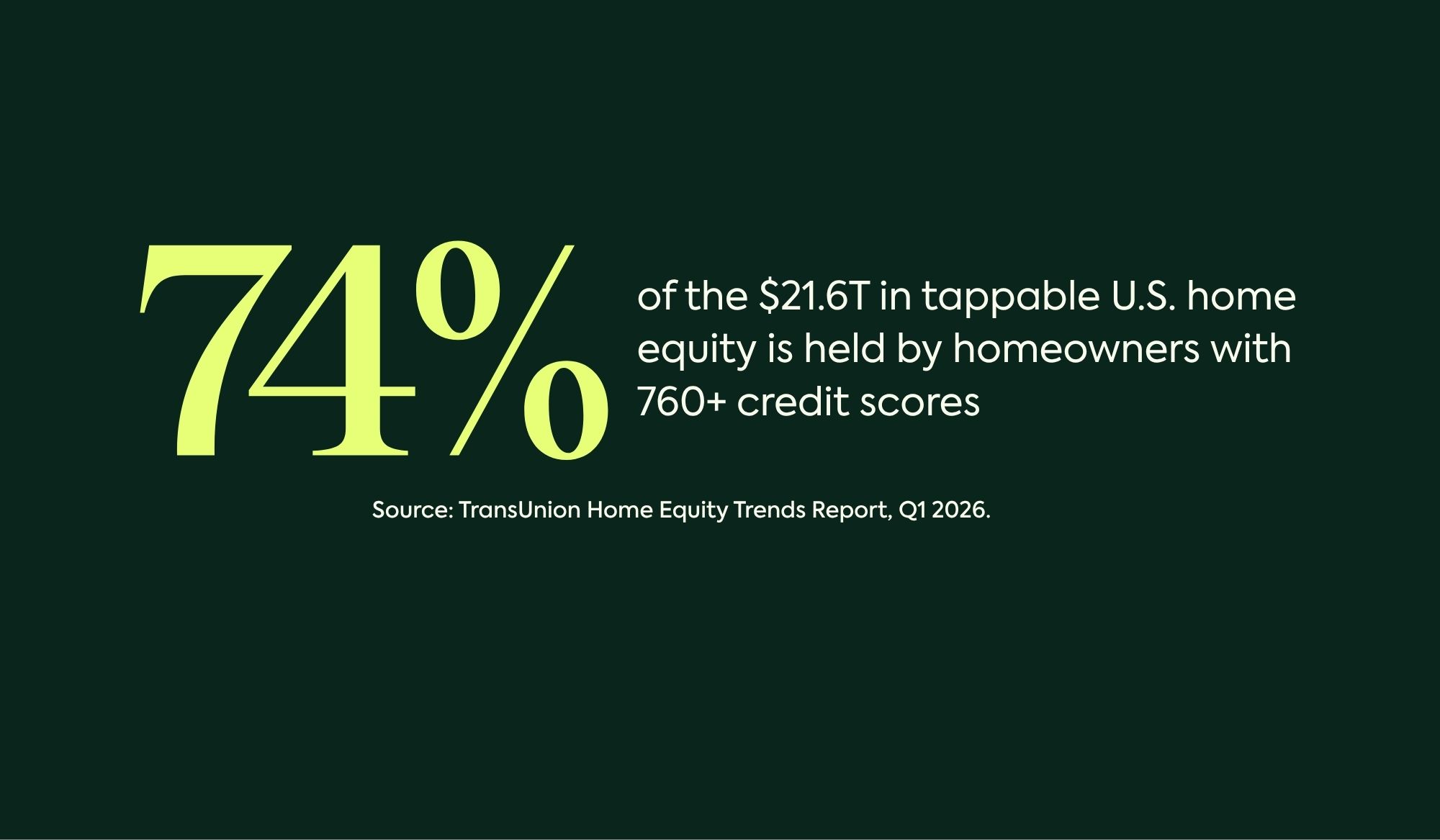

Home Equity: A Large but Underutilized Planning Asset

CHEIFS exists to separate the emotional and financial aspects of homeownership.

It allows homeowners to retain ownership and control of their home while using a portion of their home equity in a planned and intentional way —providing additional financial flexibility in decision-making.

Good planning isn’t about addressing problems after they appear. It’s about creating conditions that make thoughtful decisions easier.

Some financial products — including reverse mortgages, HELOCs, and other borrowing strategies —are often used later in life, only after other assets or income sources have been reduced.

If home equity decisions are delayed, flexibility may be limited, terms may be less favorable, and obligations may create additional pressure. This can make it harder to evaluate options fully.

Proactive planning with home equity could change that dynamic.

It can help homeowners and their families reposition a portion of net worth while timing and resources are favorable — retaining control and flexibility in planning.

The Strategic Role of Home Equity in Modern Planning

Today’s retirement landscape is defined by three realities:

1️⃣ Retirement is lasting longer than expected.

2️⃣ Taxes are likely to rise, not fall.

3️⃣ A growing share of household wealth is locked inside primary residences.

Yet many planning tools primarily focus on liquid assets, with home equity often considered as untouchable until much later in the process.

CHEIFS reframes home equity as a planning asset that can be deployed intentionally alongside cash and investments.

That opens the door to potential ways CHEIFS may be used, including:

✅ Supporting funding long-term care without liquidating portfolios.

✅ Creating retirement income buffers.

✅ Reducing tax exposure through Roth conversions.

✅ Assisting family members with housing affordability.

✅ Avoiding debt-based solutions later in life.

Most importantly, these decisions can be modeled and evaluated years in advance — supporting proactive planning opportunities.

How CHEIFS Is Structurally Different

Traditional home equity solutions rely on debt.

HELOCs and home equity loans accrue interest and create monthly payments that can reduce retirement cash flow. Reverse mortgages avoid monthly payments, but as interest accrues the balance increases over time, which could eventually consume all the borrower’s home equity.

CHEIFS was designed to avoid both outcomes.

It is a non-debt, non-recourse HEI product where Cornerstone Financing purchases a percentage of a home’s future value (“equity share percentage”) in exchange for an up-front investment payment to the homeowners. When a settlement event occurs, an equity share return (equity share percentage times the home’s then value) becomes payable from the home’s proceeds.

There are:

❗️No new monthly payments.

❗️No effective fixed term.

❗️No income qualification.

❗️Caps on the equity share percentage preserve home equity for the homeowner.

Homeowners retain ownership and management of their home during the CHEIFS term. Unlike most other popular HEI products, which have a 10-30 year set term, the CHEIFS term effectively continues until a settlement event, such as home sale, permanent move-out, or death. There are no prepayment penalties if the homeowner wishes to settle earlier. Homeowners have no personal liability; any payment that becomes due is paid from the home’s proceeds.

This allows families to plan for settlement transparently and exit when it makes sense for them.

This structure offers a different incentive alignment than traditional, debt-based home financing and provides a way to utilize home equity strategically while remaining in the home.

Before Challenges Arise

The most important insight from the New York Times article is not about scams.

It is about timing. Challenges may arise when people are faced with last-minute financial decisions.

These challenges occur when options are limited, stress is high, and liquidity is rigid — or when homeowners and their families wait until other assets are gone before thinking about home equity.

CHEIFS can help homeowners and their families work with their financial advisors to evaluate home equity earlier, under calmer conditions, with clearer visibility into trade-offs. That is what proactive financial planning can look like: not reacting better but designing better systems that avoid reactivity.

The Bottom Line

Homeownership and home equity are not the same thing. Understanding that distinction enables new ways to access home equity to manage cash flow risk without selling or taking on monthly loan payments.

CHEIFS was built to help homeowners use home equity intentionally and thoughtfully.

CHEIFS is a home equity investment agreement (or “HEI”), not a loan. To learn more about CHEIFS, including additional costs and important terms, conditions, and eligibility, please visit us at chiefs.com or call us toll-free at 1-855-GO-CHEIFS (1-855-462-4343), Mon-Fri, 8:30am to 5:30pm (ET). Or email us at [email protected].

CHEIFS is not available in all states. Cornerstone does not offer HEI products or solicit business related to properties located in New York State.

CHEIFS is offered exclusively by Cornerstone Financing LLC, and its subsidiary Domus Funding Corp. (in California only), and does business as “Domus Funding LLC” in OH and as “Domus Funding” in NH (all referred to as “Cornerstone” or “Cornerstone Financing”). Principal Office: 86 Summit Ave., Ste. 201, Summit, NJ 07901. Toll-free (855) 462-4343. NMLS #2557707, www.nmlsconsumeraccess.org/. Domus Funding Corp, CA DRE License #02248492. Not licensed in all states. Cornerstone’s HEI product is not offered under state mortgage lending licenses. For additional state licensing information, please visit cheifs.com/licensing/.

InsMark® and Wealthy and Wise+™ are service marks of InsMark LLC and are used with permission. Wealthy and Wise+™ is a financial modeling software platform owned and operated by InsMark LLC and made available to financial advisors on a subscription basis. InsMark LLC is not an agent of, or affiliated with, Cornerstone Financing, and Cornerstone Financing does not assume any responsibility or liability for Wealthy and Wise+ or for InsMark LLC’s products, services, information, or conduct.

© 2025 Cornerstone Financing LLC. “CHEIFS” is a registered service mark, and the CHEIFS logo is a service mark, of Cornerstone Financing LLC. All rights reserved.