When Home Equity Is Trapped Behind a Pay Stub

Helping asset-rich, income-constrained retirees access housing wealth when conventional underwriting screens them out

An educational article for financial advisors, retirement planners, and wealth managers.

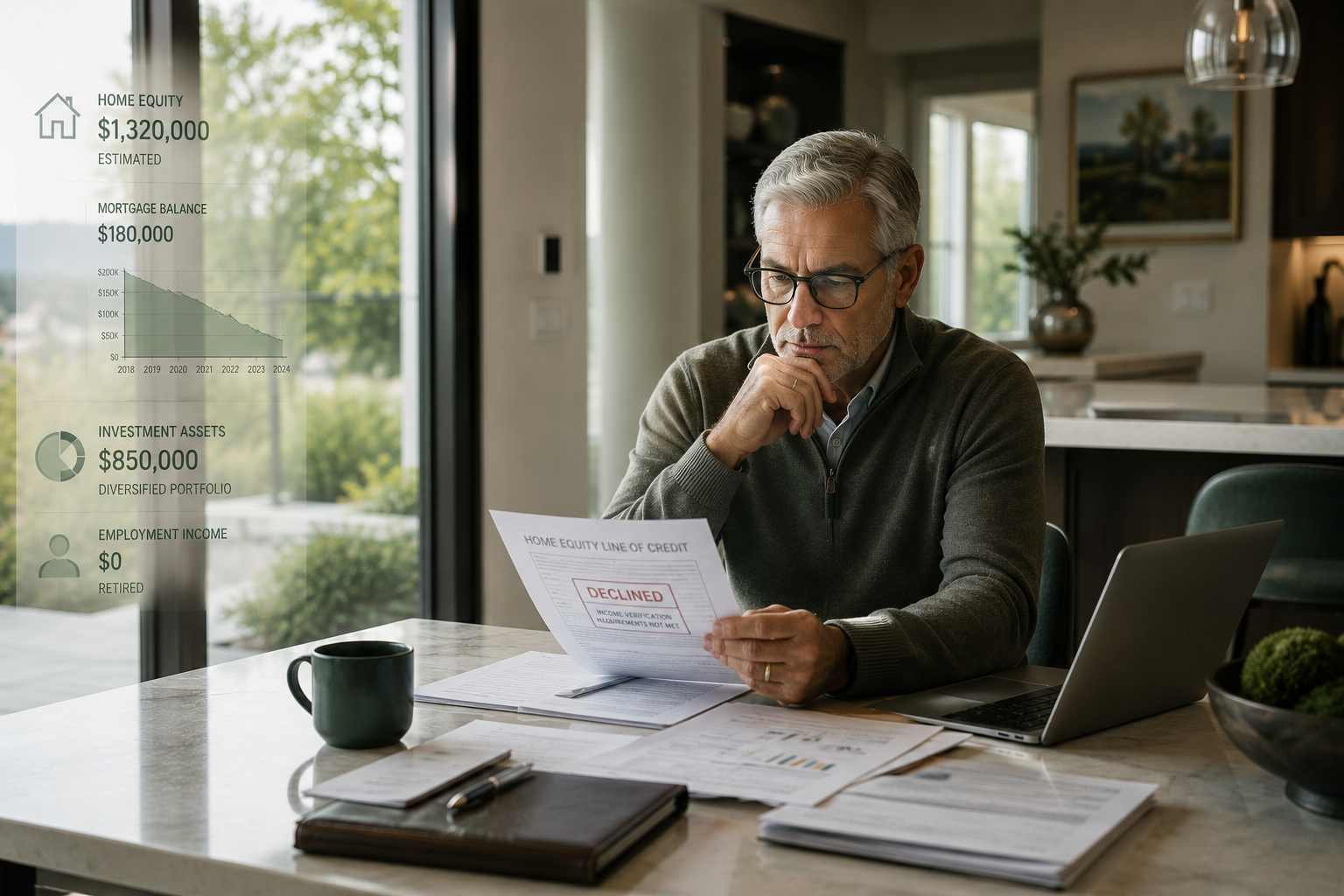

There is a quiet contradiction at the center of many retirement plans. Clients spend three or four decades building equity in a home, come to view it as one of the most stable assets on their balance sheet, and then discover, often at the worst possible moment, that the lending system was not built to let them touch it once the paychecks stop.

The pattern is familiar to advisors who work with recent retirees. A client with a paid-down mortgage, a high credit score, and ample liquid assets applies for a home equity line of credit. The application stalls, not because the numbers are weak, but because the income on the form does not come from an employer. The moment “retired” appears on the application, the conversation often changes.

This is less a credit problem than a planning problem, and it is one advisors are well positioned to get ahead of.

Why strong borrowers still get declined

Most home equity lines are underwritten around employment income. Lenders are accustomed to documenting wages through a W-2, recent pay stubs, and two years of tax returns. Retirement income, by contrast, often arrives from a mix of Social Security, pension payments, and portfolio withdrawals. Even when those sources are consistent and more than sufficient to service a new payment, internal underwriting standards can treat them as secondary or less stable.

The result is counterintuitive. A homeowner in their late sixties with substantial equity, no consumer debt, and a low prospective loan-to-value ratio can still be flagged at the income-verification stage. The denial letter rarely explains the real reason, which leaves the client frustrated and the advisor fielding a question that sits squarely between financial planning and lending.

Exhaust the conventional avenues first

Before reframing the question entirely, it is worth noting that not every lender underwrites the same way. Advisors can reasonably encourage clients to explore a few conventional paths before concluding that the door is closed.

Community banks and credit unions sometimes apply more flexibility in how they document and weight retirement income. Portfolio lenders, meaning institutions that hold loans on their own books rather than selling them into the secondary market, often have more latitude to consider a client’s full financial picture.

It is also worth asking any lender directly whether they offer asset-depletion underwriting, sometimes called asset dissipation. Under this approach, recognized within Fannie Mae and Freddie Mac guidelines for certain loan types, a lender divides a borrower’s qualifying liquid assets across a set number of months to derive a monthly income figure. A retiree with a sizable brokerage account can, under this method, generate a qualifying income that conventional employment-based underwriting would never have surfaced. Not every lender offers it, and the formulas vary, but it is a legitimate and well-established method worth confirming before assuming the answer is no.

Reframing home equity as a planning asset

When conventional access genuinely does not fit a client’s situation, the more productive conversation shifts away from “how do we qualify for a loan” toward “how does housing wealth fit into the broader plan.” This is the reframe advisors are uniquely equipped to lead.

Housing wealth is frequently the largest asset a household holds, yet it is often left out of the working plan precisely because it is seen as illiquid and access-restricted. For clients who are reluctant to draw down a portfolio during a volatile market, or who want to preserve invested assets for longevity or legacy reasons, the question of whether and how to convert a portion of home equity into usable funds becomes a genuine planning decision rather than a financing afterthought.

In certain planning scenarios, some advisors evaluate a home equity investment agreement, or HEI, as one structure within this conversation. An HEI is not a loan and not a reverse mortgage. A financial company provides the homeowner with funds today in exchange for a share of the home’s value at a future settlement event. The homeowner retains title and ownership and continues to live in and maintain the home.

CHEIFS®, offered by Cornerstone Financing, is one example of a modern HEI structure. As with any HEI, the agreement carries no new monthly payments. The homeowner remains responsible for property taxes, insurance, maintenance, and any existing mortgage payments, and the investor receives its share of the home’s value when a settlement event occurs, typically the sale, permanent move-out, or death of the homeowner. Because qualification centers on the equity in the home rather than on employment income, the structure can remain available to households for whom traditional income documentation has become the obstacle.

The tradeoff advisors should put on the table

This is not a free lunch, and the planning conversation is incomplete without saying so plainly. The structure exchanges payment flexibility today for a share of future appreciation, and if a home appreciates substantially over a long horizon, the settlement amount can be more than the upfront funds the homeowner received. The settlement figure is based on a percentage of the home’s value at the time of settlement, not on the amount advanced.

For a client on a fixed income who cannot comfortably absorb a new monthly obligation, the absence of added monthly payments and the ability to leave a portfolio untouched may be worth that potential future cost. For a client who could genuinely qualify for lower-cost conventional financing, those options deserve to be exhausted first. The advisor’s role is not to steer toward a single answer but to model the scenarios honestly: cost across different holding periods, the effect on legacy goals, and how the decision interacts with the rest of the plan.

That is the difference between a product conversation and a planning conversation. Home equity is too large an asset to leave out of the plan simply because the banking system made it inconvenient to reach. Once it is on the table as a deliberate planning input rather than a last resort, advisors can help clients weigh it the way they would any other meaningful financial decision.

Disclosures

This article is for financial professional use and for informational and marketing purposes only. It does not constitute financial, tax, or legal advice. Advisors should evaluate the suitability of all available options for each client’s individual situation, and homeowners should consult with independent, licensed financial, tax, and legal professionals for advice. CHEIFS may involve risks, fees, costs, contractual obligations, and other material considerations not appropriate for all homeowners. Homeowners and their independent advisors should carefully evaluate all available options against the homeowner’s individual financial situation, goals, and overall financial and tax strategy.

CHEIFS is a home equity investment agreement (or “HEI”), not a loan. This is not an offer or commitment. CHEIFS is subject to underwriting and approval, including property appraisal(s) and verification of credit history, property condition, title, and property insurance, among other things. The subject property may not be in foreclosure or bankruptcy. Performance of the CHEIFS agreement is secured by a mortgage or trust deed, depending on the state, in no lower than second lien priority. Minimum investment payment is $70,000. Owner-occupied, 1-2 unit residential properties only. The equity share return becomes payable upon a settlement event and is calculated as a percentage of the home’s future value, subject to the program’s cost cap. Homeowner pays an origination fee plus appraisal, title, recording fees, and other closing costs. Homeowner must occupy and maintain the property and remain current on property insurance, taxes and assessments, and payments on any other mortgages. Terms may vary and are subject to change. Additional conditions apply. Not available in all states.

Cornerstone acts for itself, as the investor, and not as an agent or broker for the homeowner or any third party. There is no agency relationship between Cornerstone and a homeowner related to the CHEIFS agreement.

Cornerstone does not offer HEI products or solicit business related to properties located in the states of NY, MN, and certain other states. Please visit cheifs.com/licensing for a list of states where CHEIFS is offered. CHEIFS is offered exclusively by Cornerstone Financing LLC, and its subsidiary Domus Funding Corp. (in California only), and does business as “Domus Funding LLC” in OH and as “Domus Funding” in NH. Principal Office: 86 Summit Ave., Ste. 201, Summit, NJ 07901. Toll-free (855) 462-4343. NMLS #2557707, www.nmlsconsumeraccess.org. CA DRE license #02248492. Not licensed in all states. Cornerstone’s HEI product is not offered under state mortgage lending licenses.

© 2026 Cornerstone Financing LLC. “CHEIFS CONVERTING HOME EQUITY INTO FINANCIAL SUCCESS” and “CHEIFS” are registered service marks, and the CHEIFS logo is a service mark, of Cornerstone Financing LLC. All rights reserved.