How CHEIFS® Could Help Parents Support First-Time Homebuyers

Over the past four decades, housing affordability for first-time buyers has deteriorated sharply.

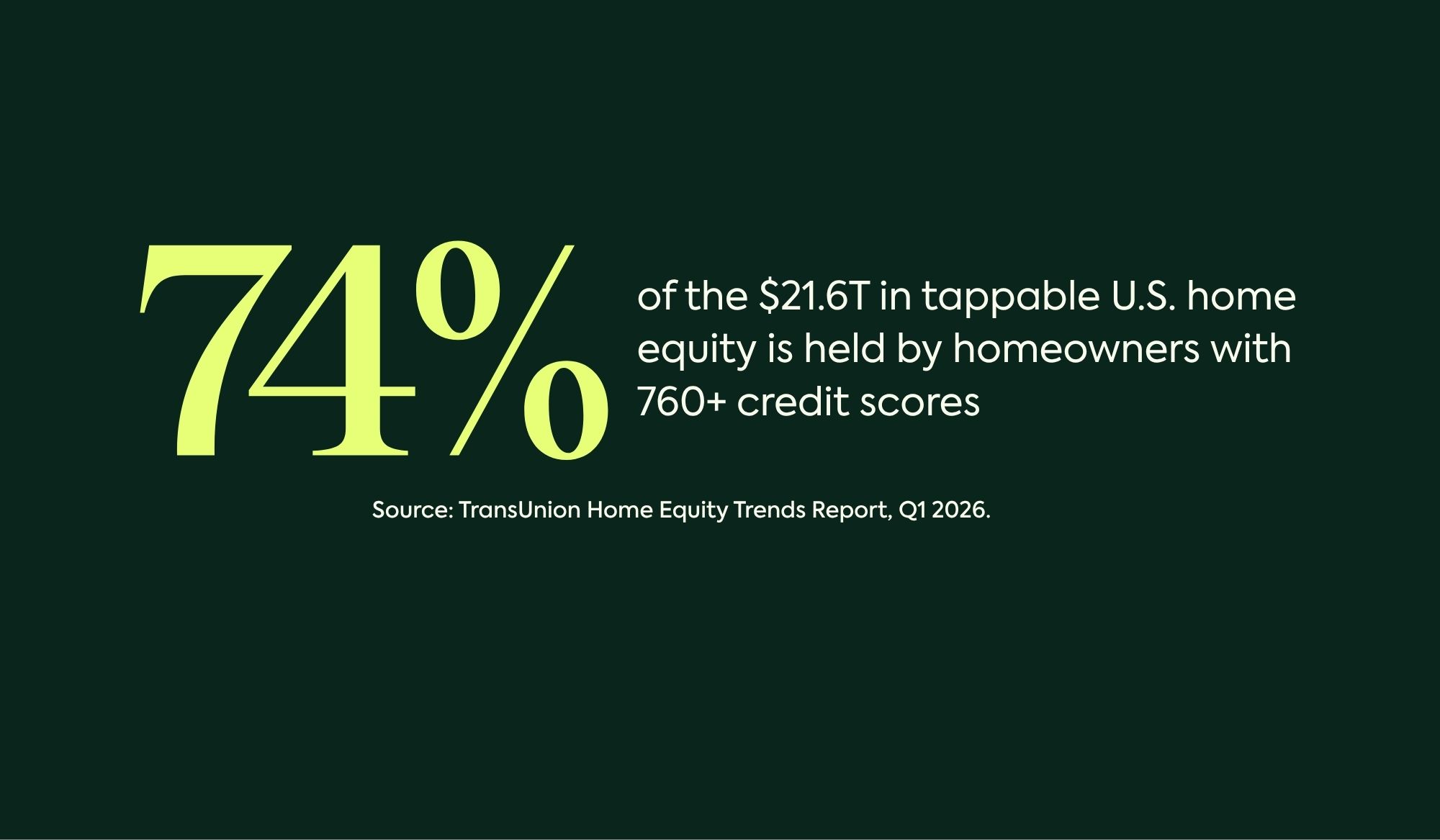

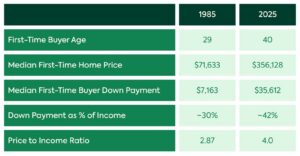

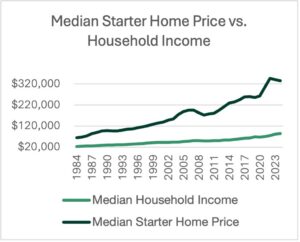

Since 1985, median starter home prices (calculated as 85% of the median home price) have increased from $71,633 to over $356,128 today, roughly a 5× increase. In contrast, the median household income grew from $23,620 to $83,730, only about 3.5×. This widening gap has made homeownership harder for younger generations than at any point in recent history. Today’s buyers face historically high prices and elevated borrowing costs, with mortgage rates hovering around 6–7%. As a result, the average first-time homebuyer is now around age 40, up from age 29 in 1985.

In 1985, a down payment of 10% was $7,163 of the median first-time home price and was often funded entirely from savings. By 2025, the same 10% down payment requires $35,612, nearly 5× higher in dollar terms. Today, savings alone rarely covers the downpayment, with savings funding about 59% and family gifts covering 22%. The down payment burden as a percentage of annual income has also increased. In 1985, a $7,163 down payment was about 30% of annual income. Today, a $35,612 down payment is approaching 42% of annual income, creating a significant barrier for younger buyers.

The home price-to-income ratio for first-time buyers, a key affordability measure, has climbed from 3.03 in 1985 to 4.26 today, highlighting how severely unaffordable the market has become. Buyers now require significantly more income compared to the 1980s, while the average age of first-time buyers has increased by 11 years, reflecting delayed homeownership driven by affordability constraints.

Parents: A New Way to Help

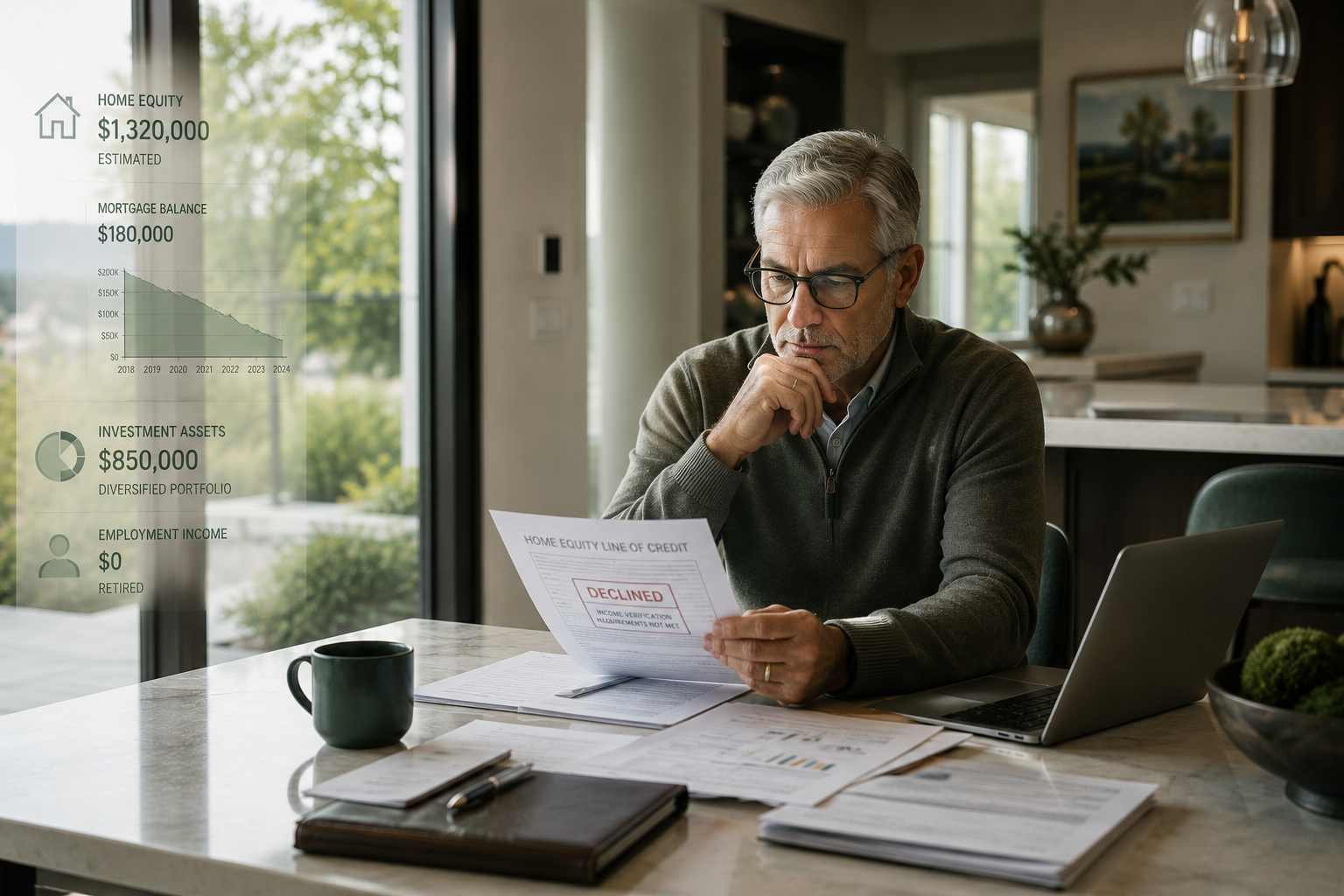

Many parents of first-time homebuyers want to help their children purchase a home during their lifetime so they can see the benefits of homeownership firsthand. However, selling investments or taking on new debt can disrupt long-term retirement plans, cash flow, and create meaningful tax consequences.

CHEIFS® offers a modern alternative for homeowners who want to help but don’t want to sell investments or take on new monthly payment obligations.

How it Works

CHEIFS is a unique home equity investment agreement (or “HEI”) offered exclusively by Cornerstone Financing (as Investor), which converts a portion of home equity into liquidity, without requiring monthly payments or refinancing any existing first mortgage.

The homeowner sells a percentage interest in their home’s future value to the Investor in exchange for an up-front investment payment, while continuing to own and occupy the home. There is no fixed term or required monthly payment to the Investor until a settlement event occurs, such as the homeowner’s sale of the home, permanent move-out, or death. At that time, the Investor receives a payment (“equity share return”) equal to its percentage interest multiplied by the home’s future value at the time of settlement event. However, the equity share return will not exceed an annualized cost cap starting at 12.99% on the investment payment, compounded annually. Homeowners may choose to settle early without a prepayment penalty. The equity share return is paid from the home’s proceeds; the homeowner has no personal liability. See below for additional costs and details.

Visit CHEIFS.com today to learn more and to try our CHEIFS calculator.

This material is for informational and marketing purposes only and does not constitute financial, tax, or legal advice. Homeowners should consult a licensed independent financial advisor, accountant, or legal advisor before entering into any HEI.

CHEIFS is a home equity investment agreement (“HEI”). The homeowner receives an up-front investment payment from Cornerstone (as Investor) based on a percentage of the home’s starting appraised value. Under the CHEIFS Prime program, for each 1% of that starting value the homeowner receives, the Investor receives an equity share of 2.25% of the home’s future value, but the equity share will not exceed an annualized cost cap of 12.99% on the investment payment, compounded annually. Investor receives payment of its equity share return upon a settlement event, typically the homeowner’s sale of the home, permanent move-out, or death. Minimum starting home value is $315,000 (if no existing mortgage) for a primary residence. Other programs and terms apply based upon starting home value and available equity. Homeowner to pay an origination fee of up to 2.99% of the investment payment or $2,000, whichever is more, plus credit report, appraisal, title, closing fee, and other closing costs, which may be deducted from the investment payment or paid separately. The homeowner’s obligations are secured by a mortgage or deed of trust recorded against the home in no lower than second lien position. Homeowner must continue to occupy, maintain, and insure the home and pay timely all property taxes, assessments, HOA, and any senior mortgage payments. Additional fees, terms, and conditions apply. This is not an offer or commitment. Subject to underwriting and approval. Terms may vary and are subject to change. Not available in all states. Not offered for properties or to homeowners located in New York or Minnesota. Visit cheifs.com for additional details.

CHEIFS is offered exclusively by Cornerstone Financing LLC, a New Jersey limited liability company, and its affiliates (together, “Cornerstone” or “Cornerstone Financing”). NMLS #2557707 (www.nmlsconsumeraccess.org). Domus Funding Corp, CA DRE Lic. #02248492. Not licensed in all states. For additional state licensing information, please visit us online at cheifs.com/licensing.

© 2026 Cornerstone Financing LLC. All rights reserved.