Home Equity on Paper, Home Equity in Hand: The Realization Gap Reshaping Retirement Planning Conversations

New research highlights a hidden discount in late-life home sales, a quiet erosion of housing wealth through rising carrying costs, and a planning question worth asking earlier.

By most measures, home equity has never been a larger force on the retiree balance sheet. According to the NRMLA/RiskSpan Reverse Mortgage Market Index, housing wealth held by homeowners age 62 and older reached a record $14.66 trillion in the third quarter of 2025, the highest level since the index began tracking in 2000. Total U.S. homeowner equity in residential real estate, according to Federal Reserve data, sits near $35 trillion. By any measure, the American homeowner is sitting on a historic accumulation of housing wealth.

But for a meaningful number of retiree households, the number on the balance sheet may overstate the number that can actually be realized at the moment of need. A growing body of research suggests that the path from “home equity on paper” to “home equity in hand” is more friction-laden, and more expensive, than retirement plans typically account for. The implications are most acute for households where the primary residence represents a disproportionate share of net worth.

A recent piece in HousingWire summarized the issue plainly: retirees may be counting more heavily on their homes as retirement safety nets than the underlying math supports. That headline rests on a more substantial body of research worth examining carefully, because the planning implications are not abstract.

The Realization Gap

In financial planning, the gap between an asset’s stated value and what an owner can actually obtain for it at the point of need is a familiar concept. For securities, the gap is usually small, captured in bid-ask spreads and execution costs. For real estate, particularly for retirees, the gap can be considerably wider, and the components are well-documented.

The realization gap, as a planning concept, captures three things at once. The discount that older homeowners tend to absorb when they sell. The carrying costs that quietly erode housing wealth in the years before a sale. And the time, friction, and uncertainty involved in converting a home into liquid capital at the moment a household actually needs it.

Each of these components is documentable. Together, they shape how home equity should be evaluated as a planning asset, not simply whether the home equity exists, but on what terms it can be brought into a financial plan.

What the Boston College Research Actually Found

The clearest evidence of the late-life realization discount comes from the Center for Retirement Research at Boston College. A 2025 study by Philip E. Strahan and Song Zhang, which linked roughly 10 million repeat home sale records to voter registration data to estimate seller age, found that the age gap in home sale returns is real, persistent, and widening.

According to the brief, an 80-year-old seller realizes approximately 0.5 percent per year less than a 45-year-old seller. Over the mean U.S. holding period of 11 years, that compounds to roughly a 5 percent lower sale price. On a home priced near the national median of $405,400, the discount works out to approximately $20,000 in foregone proceeds, and the gap widens with each additional year of seller age. The pattern is pervasive across the country, with the researcher’s noting deviations from the general trend in only three small states.

Two factors explain most of the discount.

First is the condition of the home itself. Coverage in CNBC and the underlying research note that homes sold by older owners are more likely to carry signs of deferred maintenance or outdated finishes. Younger owners’ listings reference upgrades such as new roofs or remodeled kitchens at higher rates; older owners’ listings disproportionately include phrases such as “as-is” or “fixer-upper.” Property condition alone explains a meaningful share of the age gap in returns.

Second is sales-channel choice. The CRR research found that sellers aged 76 and older were 2.3 percent more likely to sell off the Multiple Listing Service entirely and 2.7 percent more likely to sell directly to investors. Both pathways are associated with lower sale prices because they limit competitive bidding pressure. Sellers using off-MLS or investor channels receive returns that are approximately 1 percent lower than middle-aged sellers using the same channels, the study found.

Supporting data from the National Association of REALTORS® 2025 Home Buyers and Sellers Generational Trends report reinforces the same dynamic. Among sellers in the 79-to-99 age band, 44 percent had lived in their home for 21 years or more, and 15 percent sold their home for less than 90 percent of the listing price, the largest share of any age group surveyed.

The takeaway for advisors is not that older homeowners are being misled, although certain pockets of the market do warrant concern. The more important takeaway is that the physical, logistical, and emotional realities of selling a long-held home in one’s 70s or 80s tend to produce a different outcome than the appraised value or the public estimate suggests. That outcome is largely predictable in advance, and largely plannable around.

Why Carrying Costs Are Compounding the Gap

The realization discount at the point of sale is only part of the picture. In the years leading up to a sale, retiree homeowners are absorbing carrying costs that have escalated faster than most retirement plans assumed.

Homeowners insurance is the clearest example. According to Insurify’s 2026 home insurance outlook, the average annual premium has climbed approximately 46 percent since 2021, nearly three times the pace of inflation, and is projected to reach about $3,057 in 2026. Matic’s 2026 trends report finds that household insurance costs now represent roughly 9 percent of a typical homeowner’s monthly mortgage payment, the highest share on record. Average deductibles climbed an additional 22 percent in 2025 as carriers shifted more financial responsibility to homeowners.

For homeowners in coastal or wildfire-exposed regions, the arithmetic is sharper still. Florida’s average premium approaches $8,500, more than double the national average. Following the January 2026 Los Angeles wildfires, California carriers are projecting significant additional increases. Matic’s analysis estimates that climate-related insurance pricing has reduced home values by approximately $20,500 in the top 25 percent of catastrophe-exposed homes, and by $43,900 in the top 10 percent.

Property taxes, HOA fees, and routine maintenance costs follow similar trajectories. For retiree households on relatively fixed incomes, these recurring expenses compress the practical value of housing wealth in two ways. They reduce the cash available to maintain the home in market-ready condition. And they accelerate the very deferred-maintenance dynamic that produces the late-life sale discount documented by the CRR research.

In other words, the conditions that cause older homes to sell for less are partially driven by the same cost pressures that make those homes more expensive to own each year. The realization gap does not open at the closing table. It opens slowly, over years.

The Planning Question: When Should Home Equity Be Accessed, and How?

For financial advisors, this body of research raises a question that does not appear often enough in retirement income conversations. If a portion of the realization gap is foreseeable, driven by predictable patterns of carrying costs, deferred maintenance, and late-life sale dynamics, then the timing and mechanism of accessing home equity deserve the same planning rigor that portfolio withdrawal strategies receive.

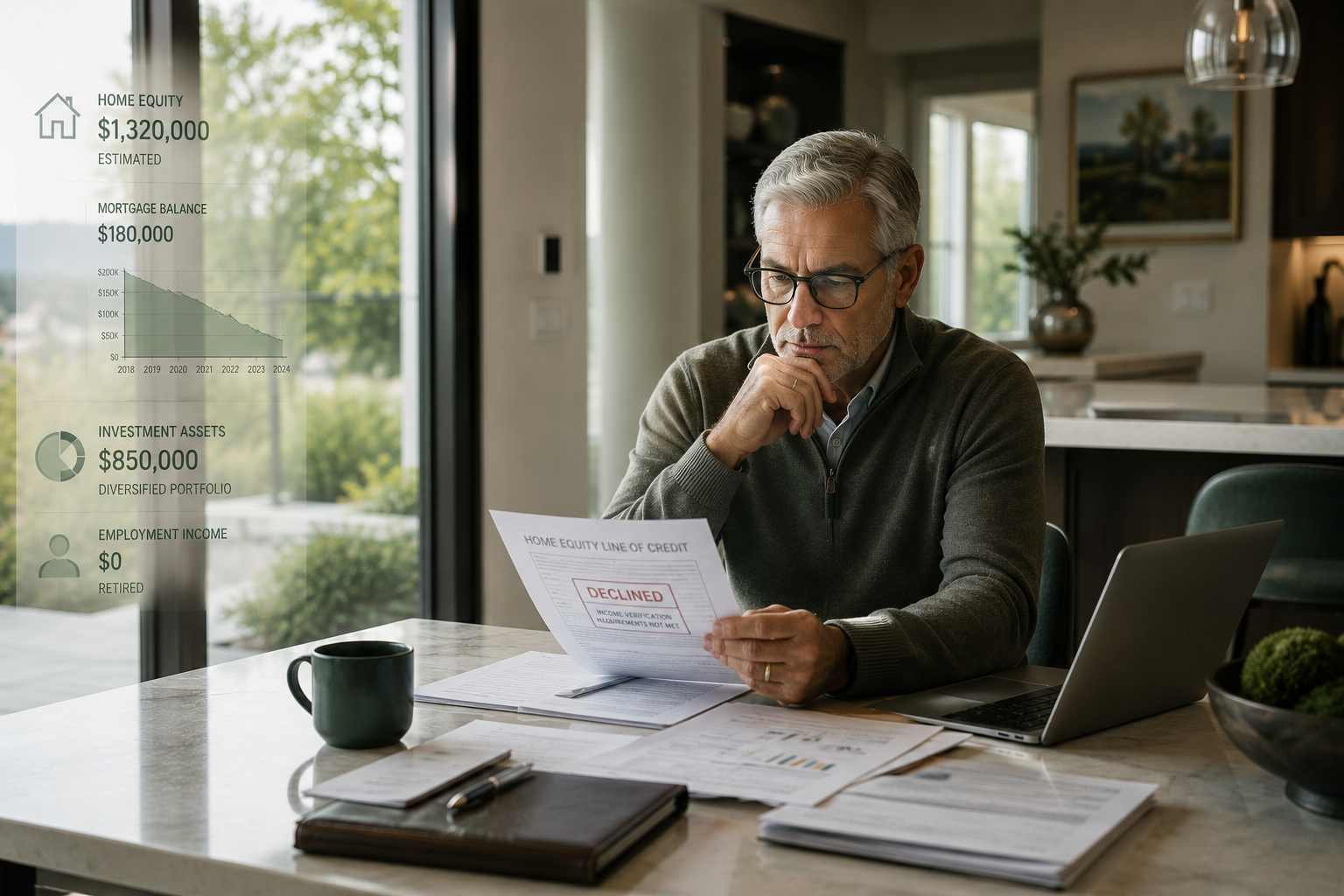

The conventional approach has been to treat the home as a residual asset. It is lived in for as long as practical, sold near the end of life, and the resulting proceeds are either spent down in late retirement or passed to heirs. That approach is not wrong, but it leaves the realization gap entirely uncoordinated with the rest of the financial plan. The sale happens when life circumstances dictate, often under time pressure, often after years of deferred upkeep, and often into a market that is not the one the plan assumed.

A more coordinated approach involves evaluating, well before the household has to act, whether and how a portion of home equity can be brought into the planning conversation earlier. The question becomes whether the household has the option to convert some portion of housing wealth into liquidity at a point when it has time, leverage, and choice, rather than under the pressure of a forced sale or a health event.

Advisors are now evaluating that question explicitly. Not whether home equity will be a planning asset, but when and through what mechanism it should become one.

Why the Home Equity Access Conversation Has Been Shifting

The home equity market itself has been changing in ways that make this planning question more answerable than it was a decade ago.

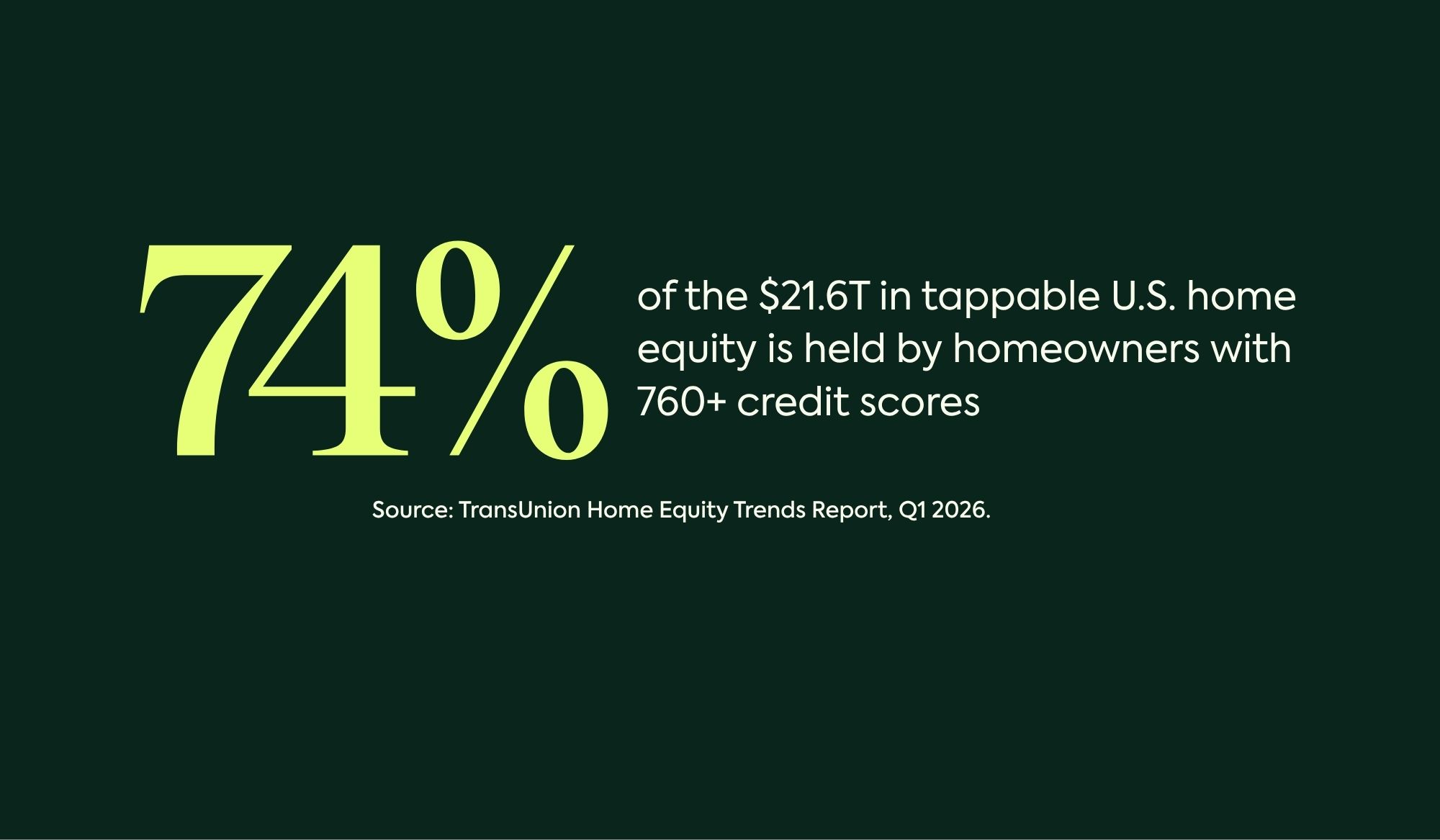

Activity through 2025 confirms the trajectory. According to Cotality’s 2025 origination data, open- and closed-end home-equity lending advanced to roughly 2.2 million units totaling $311 billion last year, up from approximately 2.1 million units totaling $270 billion in 2024. HELOC originations alone reached 1.5 million units for $271 billion in 2025, compared with 1.4 million units for $230 billion the prior year, with HELOC share of home-equity lending widening to 87 percent. TransUnion’s Q4 2025 Credit Industry Insights Report described home-equity originations as having posted a sixth straight quarter of growth, with HELOC originations alone rising nearly 16 percent year-over-year in the third quarter. Tappable home equity across the 104 million U.S. homeowner base reached $21.4 trillion at year-end 2025, according to the same report. ICE Mortgage Monitor data put 2025 second-lien home-equity withdrawals at $116 billion, the highest annual level since 2007.

The growth is not only on the volume side. The structural mix of who is originating has changed materially. Between 2023 and 2025, HELOC originations at large banks rose 7 percent, while regional banks recorded 20 percent growth, credit unions advanced 8 percent, and fintech lenders surged approximately 140 percent as digital-first underwriting models reduced the time and friction of approval. Alternative HEI structures have also gained ground, with the top five HEI originators collectively reaching roughly $600 million per month of origination as of mid-2025. The range of structures available to homeowners is the broadest it has been in the modern era of the market.

Borrower behavior is reinforcing the trend. A 2025 TD Bank survey found that nearly three-quarters of homeowners plan to remain in their current homes over the next two years, with 58 percent citing a favorable existing mortgage rate as a key reason not to sell. These homeowners are not disengaging from home equity. They are looking for ways to access it without sacrificing the financial positions they have built.

A Structural Alternative Worth Understanding

A home equity investment agreement, often referred to as an HEI, operates differently from traditional financing. It is a contract under which an investor provides the homeowner with a lump sum today in exchange for a contractual interest in a portion of the home’s future value. Settlement occurs at a defined future event, typically the sale of the home, the homeowner’s permanent move-out, or the homeowner’s death, depending on the specific HEI structure.

The mechanical differences from traditional financing matter for planning purposes. Under most HEI structures, there are no new monthly payments and no monthly interest accrual. Homeowners remain responsible for property taxes, insurance, maintenance, and any existing mortgage payments. The investor’s return is realized when settlement occurs and is calculated based on the contractual terms, which commonly include a percentage of the home’s value at settlement and may be subject to a cost cap. Underwriting typically does not require income verification or debt-to-income evaluation in the same way a traditional loan does. The homeowner retains title and ownership of the home, subject to the terms of the agreement, including contractual conditions on sale, transfer, or refinance.

For advisors thinking about the realization gap, the relevant feature of an HEI is structural. It allows a household to convert a portion of housing wealth into deployable capital at a point of choice rather than under the time pressure of a late-life sale. The proceeds can be used to fund retirement income strategies, insurance and long-term care planning, the tax cost of a Roth conversion, portfolio preservation during volatile markets, or other planning needs that arise before the home is ever sold.

CHEIFS, which stands for Converting Home Equity Into Financial Success, was developed by Cornerstone Financing as an HEI structure designed for integration into broader financial planning. CHEIFS has no effective fixed term (in years) and settles when a contractual settlement event occurs, typically the homeowner’s sale, transfer, or move-out of the home, or death. It is non-recourse, meaning the homeowner has no personal liability beyond the property itself. There is no age minimum, no income or employment requirement, and no new monthly payments. Homeowners remain responsible for property taxes, insurance, maintenance, and any existing mortgage payments. The Cornerstone investment payment is generally not treated as taxable income upon receipt; however, there may be future tax implications of the transaction, for example upon home sale or other settlement, and any client should consult a qualified tax advisor regarding their specific situation. Additional details on how the CHEIFS structure works is available at cheifs.com.

The purpose of including this here is not to position any single product. It is to note that the structure exists, that institutional capital and securitization markets around HEIs have matured substantially over the past several years, and that for advisors evaluating how housing wealth fits into a planning conversation, the structural options today are broader than they were five years ago.

Reframing the Concentration Question

For mass affluent retiree households, the primary residence is not just a large asset on the balance sheet. It is typically a concentrated one. According to Federal Reserve Survey of Consumer Finances data, the primary home represents the single largest asset category for the majority of households in the 55-to-74 age band, often accounting for 30 to 50 percent of total net worth and substantially more for those who have paid off the mortgage.

In any other category, an asset of that size would prompt a portfolio-level conversation about concentration. For housing, that conversation rarely happens. The home is generally treated as exempt from the diversification logic that applies to the rest of the household’s holdings.

The realization-gap research suggests the cost of that exemption is higher than it appears. A household carrying 40 percent of its net worth in a single, illiquid, late-life-discounted, climate- and insurance-exposed asset is, by any portfolio measure, holding a level of idiosyncratic risk that would rarely be tolerated in a brokerage account.

This is where the timing of accessing home equity becomes a different kind of conversation. Converting a portion of housing wealth into other forms of capital earlier rather than later does two things at once. It allows the household to deploy that capital for planning purposes while the home is still in market-favorable condition, the homeowners are still in a position to make decisions on their own terms, and the underlying value reflected on the balance sheet has not yet been compressed by the realization-gap dynamics documented earlier in this article. And it reduces the household’s forward exposure to any single property’s future price movement. Capital monetized today is no longer concentrated in that home, regardless of what happens to that home’s value tomorrow.

This is not the same as predicting that home prices will decline. It is to recognize that for a household carrying disproportionate exposure to a single residence, the question of how much concentration to maintain at the moment of greatest vulnerability, typically late retirement, frequently with deferred maintenance and rising carrying costs, deserves the same scrutiny as any other concentration question in a financial plan.

The structural options available today address this dimension differently. Traditional financing options, including HELOCs, home equity loans, and cash-out refinances, provide liquidity but leave the underlying ownership concentration intact and add a recurring debt-service obligation against the same concentrated asset. A home equity investment agreement converts a portion of the home’s current value into capital that, once received, is no longer subject to the home’s subsequent price trajectory. The household’s forward exposure to home price movement is reduced in proportion to the share of value monetized. For households where the residence is the dominant asset, that distinction matters.

What Advisors Can Do With This

For financial advisors and insurance professionals working with mass affluent retiree households, the implications of the realization-gap research are practical.

Run the calculation. For clients where the primary residence represents a significant share of total net worth, often 30 percent or more, model the household’s retirement plan both with and without a realistic discount applied to home value at sale. The CRR research suggests a 5 percent planning haircut is a defensible starting point for households where a sale is likely to occur after age 75. In high-cost states with sharp carrying-cost inflation, the haircut may need to be larger.

Ask about timing. Whether the household intends to sell at all is itself a planning question. For households planning to remain in place, accessing home equity without a sale becomes the central question, and the available mechanisms vary considerably in cost, friction, and structural impact on the rest of the plan. The conversation should start before the household is under pressure to act.

Identify the funding blockages elsewhere in the plan. Clients who have declined long-term care coverage, deferred Roth conversions, or under-funded permanent life insurance often cite the same set of reasons: they do not want to liquidate investments, drain cash reserves, or take on debt with monthly payments. Home equity, accessed through the right structure, can sometimes resolve those blockages without disturbing the underlying constraints.

Document the realization assumption. Many retirement plans implicitly assume the home will be sold at appraised value at some point in the future when the household no longer needs it. The research suggests that assumption is generous more often than not. Whether the gap is closed by selling earlier, accessing home equity through a different mechanism, or holding additional liquidity elsewhere in the plan, the underlying assumption itself deserves to be made explicit and stress-tested.

The Broader Principle

The home equity conversation in financial planning is expanding well beyond the familiar questions of rate, term, and monthly payment. It is increasingly a conversation about the relationship between an asset’s stated value and its realized value, and about the planning choices that determine which of those numbers ends up funding the rest of the financial plan.

For decades, the home has been the largest single asset on the typical American retiree’s balance sheet, and also one of the least intentionally planned. The research now emerging on late-life sale dynamics, on the compounding effect of insurance and carrying costs, and on the broader structural alternatives available in the home equity market suggests that the cost of leaving that asset unplanned is higher than many advisors and households have assumed.

The opportunity is not to position housing wealth as the answer to every planning question. It is to recognize that the way and the timing of accessing it shape what the household actually receives. Home equity on paper is not home equity in hand. For mass affluent retiree households, closing that gap thoughtfully, and well in advance of the moment it matters, may be one of the more consequential planning conversations available today.

Sources

- NRMLA/RiskSpan Reverse Mortgage Market Index, Q3 2025 release. Senior housing wealth (homeowners 62+): $14.66 trillion. National Reverse Mortgage Lenders Association and RiskSpan, January 2026.

- Federal Reserve / FRED, Series OEHRENWBSHNO. Total U.S. homeowner equity in residential real estate, approximately $35 trillion (2025).

- Center for Retirement Research at Boston College. Philip E. Strahan and Song Zhang, “Why Do Older Sellers Get Less Money for Their Homes than Younger Sellers?” Issue Brief, 2025–2026.

- CNBC, “Home sellers start getting lower prices at 70, research shows,” February 14, 2026.

- National Association of REALTORS®, 2025 Home Buyers and Sellers Generational Trends report.

- Insurify, 2026 Home Insurance Price Projections. Average premium projected to reach $3,057 in 2026; 46 percent cumulative increase since 2021.

- Matic, 2026 Home Insurance Predictions report, December 2025. Insurance share of mortgage payment at record 9 percent; deductibles up 22 percent in 2025.

- Cotality, 2025 full-year home equity originations data, reported via HELN News, April 2026. Total open- and closed-end home-equity lending: 2.2 million units / $311 billion in 2025 (vs. 2.1 million / $270 billion in 2024). HELOC originations: 1.5 million units / $271 billion; 87 percent share of home-equity lending.

- TransUnion, Q4 2025 Credit Industry Insights Report. Home-equity originations posted sixth consecutive quarter of growth; HELOC originations +15.8 percent year-over-year in Q3 2025; total tappable home equity at $21.4 trillion among 104 million U.S. homeowners as of Q4 2025.

- ICE Mortgage Monitor, 2025 data. Second-lien home-equity withdrawals reached $116 billion in 2025, the highest annual level since 2007. Total U.S. home equity at approximately $16.9 trillion heading into 2026.

- Federal Reserve, Survey of Consumer Finances. Primary residence as share of total household net worth by age cohort.

- TD Bank, 2025 Homeowner Sentiment Survey.

- HousingWire, “Retirees counting on home equity may face financial shortfalls,” May 12, 2026.

About Cornerstone Financing

Cornerstone Financing offers CHEIFS® (Converting Home Equity Into Financial Success), a home equity investment agreement developed for integration into holistic financial planning. CHEIFS is offered through advisor and platform partners and is designed to help mass affluent homeowners and their advisors evaluate home equity as a planning asset alongside investment portfolios, retirement income strategies, insurance planning, and tax management. For more information on how CHEIFS is structured, visit cheifs.com or cornerstonefinancing.com.

This article is intended for educational and informational purposes for financial professionals. It does not constitute legal, tax, or investment advice, and does not constitute a recommendation regarding any specific financial product. Home equity investment agreements involve the exchange of future property appreciation for current capital and may not be appropriate for all clients. Specific planning recommendations should be made only in consultation with qualified legal and tax advisors based on individual client circumstances. CHEIFS® is a registered offering of Cornerstone Financing.