Rate-Locked and Asset-Rich: The Planning Problem Hiding Inside a 3% Mortgage

The cultural argument that homeownership has become a trap is loudest among people who do not own homes. A quieter, more consequential version of it is unfolding among those who do, and it is reshaping a corner of advisory work.

There is a popular argument circulating right now, amplified across podcasts and social feeds, that owning a home has become a kind of jail. The case is familiar. Homes are expensive to maintain, a single repair can cost thousands, ownership ties a household to one place and one job market, and over nearly all long-term stretches a diversified investment portfolio has outpaced home-price appreciation. The loudest version of this argument tends to come from younger adults who do not yet own and are weighing whether they ever should.

There is a quieter version of the same argument, and it deserves more attention from financial professionals, because it is coming from the opposite group. It is coming from people who already own, who did everything conventionally right, and who now find themselves comfortable on paper yet oddly constrained in practice. They locked in a mortgage rate they may never see again. They watched their equity climb. And somewhere along the way they discovered that the very thing that made their balance sheet look healthy also made it harder to move, to adapt, or to put that wealth to work. The flexibility the renters are chasing is, in many cases, the same flexibility these owners feel they have quietly given up.

That tension is not a real-estate story. It is a planning story. And for advisors, it is taking the shape of a distinct client segment that did not exist at this scale a few years ago.

The most valuable mortgage in modern history

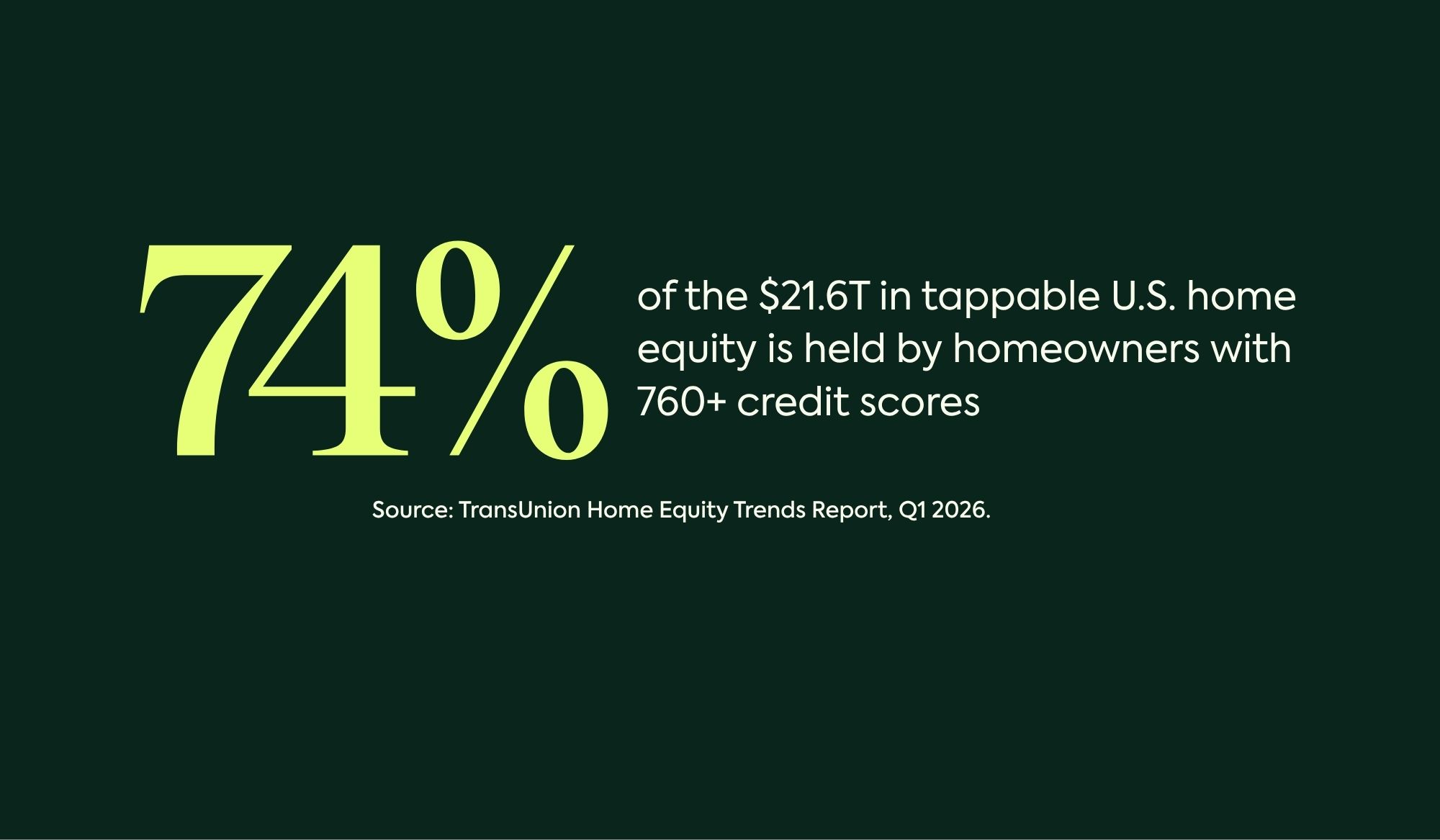

To understand the segment, start with the “asset” on the other side of it. During the 2020 to 2022 period, tens of millions of households either bought or refinanced into fixed mortgage rates that, by any historical measure, were extraordinary. That window has now closed, and the data shows just how far on the right side of it those borrowers sit.

According to Federal Housing Finance Agency data analyzed by Realtor.com, roughly half of outstanding U.S. mortgages, about 51.5% as of the third quarter of 2025, still carry a rate at or below 4%, and close to 69% sit at or below 5%. The average rate on existing mortgages is around 4.4%, well beneath the rates available to anyone shopping for financing today. For a sense of the gap, Realtor.com estimates that a typical homeowner who moved would face roughly $1,000 more in monthly housing costs, even for a comparable home, simply because the new loan would be priced at current rates.

The distribution is shifting, but slowly. In the third quarter of 2025, the share of mortgages carrying a rate of 6% or higher (about 21%) edged past the share carrying a rate below 3% (about 20%) for the first time, a quiet milestone that economists flagged as a turning point. Even so, the center of gravity remains striking: most American homeowners with a mortgage are paying a rate that no longer exists in the market. For them, that loan is not a liability in the ordinary sense. It is one of the most valuable financial instruments they will ever hold.

Which is precisely why so few of them are willing to let it go.

When a rate advantage becomes a mobility problem

Economists have a clinical name for the behavior: the lock-in effect. Households with below-market mortgages stay put rather than trade a cheap loan for an expensive one, and the cumulative result has reshaped the housing market. Home turnover fell to about 2.8% in 2025, meaning only 28 of every 1,000 homes changed hands, the lowest rate in roughly three decades, per a Redfin analysis. Existing-home sales in 2024 sank to their weakest level since 1995, and 2025 essentially matched it.

The effect extends well beyond housing inventory. The Harvard Joint Center for Housing Studies reported that overall household mobility fell to 11.2% in 2024, the lowest figure on record in the American Community Survey, with the decline driven primarily by homeowners staying in place. Research from the National Bureau of Economic Research has estimated that lock-in reduced mobility among mortgaged households by roughly 16% in 2022 and 2023, while a Federal Housing Finance Agency study attributed a 57% reduction in home sales to the same dynamic.

The shorthand that has emerged for this, in financial commentary and increasingly in client conversations, is the golden handcuff. The phrase captures something real. The low rate is genuinely valuable, and it is genuinely confining. A household can recognize both truths at once and still feel stuck between them.

The cost most plans overlook

The mobility cost is the visible one, the part that makes headlines and frustrates would-be sellers. There is a second cost that is easier to miss and, for planning purposes, often more consequential. The same decision that froze a household in place also tends to freeze a large and growing share of its net worth.

Consider the arithmetic of the last several years. Home prices rose sharply, climbing more than 50% over a six-year span by some national measures, while the cheap fixed mortgage made borrowing against that appreciation feel unappealing and selling feel even worse. The result, for millions of households, is a balance sheet increasingly concentrated in a single illiquid asset, an asset they have a strong financial incentive never to disturb. Equity accumulates. Options narrow. The wealth is real, and for day-to-day purposes it may as well not exist.

This is where the renter’s complaint and the owner’s reality converge. The younger skeptic argues that a home ties up capital and limits freedom of movement. The rate-locked owner, having built substantial equity, often experiences exactly that, only with far more at stake. The handcuff, in other words, cuts in two directions. It limits where a household can live, and it limits what a household can readily access.

A segment, not a scenario

For advisors, the analytically useful step is to stop treating these households as a collection of one-off situations and start recognizing them as a segment with shared characteristics. The profile is consistent: little or no mortgage, or a very low fixed-rate one; meaningful and often appreciated home equity; frequently at or approaching retirement; and, notably, a track record of financial discipline. These are not households in distress. They are households whose strongest financial decision has produced an unintended side effect.

Framed that way, a familiar set of planning questions takes on a sharper edge. How much of this client’s net worth is concentrated in the residence, and is that concentration intentional? What happens to liquidity if a long-term care need, a tax event, or a family obligation arrives while the bulk of the household’s wealth sits inside the home? And is the instinct to treat home equity as untouchable a sound plan, or simply an artifact of how attached the household has become to a mortgage rate? Some advisors are beginning to evaluate these households as their own planning category, with their own diagnostic questions, rather than folding them into general retirement-income work.

Separating the rate decision from the liquidity decision

When a client in this position needs liquidity, the conventional levers all share a flaw. Selling surrenders the home and the rate together. Refinancing replaces a 3% obligation with one priced at today’s levels, the precise outcome the household has spent years avoiding. Borrowing through a home equity loan or line of credit layers a new monthly payment onto a balance sheet that was built, deliberately, to avoid taking on more debt. In each case, addressing the liquidity problem reintroduces the very thing the low rate was protecting.

The conceptual move that some planners are making is to treat the rate decision and the liquidity decision as separate questions rather than a single bundled one. The premise is straightforward, and it is one we have written about before in a different context: homeownership and home equity are not the same thing. A household can value its home, its rate, and its sense of permanence while still asking, calmly and in advance, whether some portion of the equity might be repositioned as a planning resource rather than left dormant until circumstances force the issue.

Where newer home equity structures enter the conversation

Traditional options for accessing home equity, including home equity loans, lines of credit, cash-out refinancing, and reverse mortgages, each have their place and their own structures and tradeoffs, and many households and their advisors will conclude that one of them fits. They are not the subject here. What is worth noting is that a newer category has emerged that approaches the question from a different angle.

A home equity investment agreement, or HEI, is a non-recourse arrangement in which an investor provides an up-front payment in exchange for a share of the home’s future value, rather than charging interest or requiring monthly payments. CHEIFS®, offered by Cornerstone Financing, is one example of a modern HEI structure. Under it, the homeowner receives an up-front investment payment and retains ownership and occupancy of the home, with no new monthly payments to the investor. The investor’s equity share return becomes payable only at a future settlement event, such as a sale, a permanent move-out, or death, and is calculated as a percentage of the home’s value at that time.

For the rate-locked household, the relevant feature is conceptual rather than promotional: a structure of this kind does not disturb the existing first mortgage and does not add a monthly payment, which means the liquidity question can, be addressed without unwinding the rate the household has worked to keep. Whether any such structure fits a given household depends entirely on that household’s circumstances, goals, and overall financial and tax picture, which is a determination for the homeowner and their independent advisors to make. The point for planning purposes is simply that the menu of ways to think about home equity is wider than it was a few years ago, and that some advisors are now putting these structures on the table as one option to be modeled and compared against the alternatives.

The case for asking the question early

The lock-in effect is loosening, but at a glacial pace. Forecasters expect mortgage rates to broadly stay the same through 2026, and the share of ultra-low-rate loans has taken years to erode by even a few percentage points. For most rate-locked households, the handcuff is not coming off on its own anytime soon. That makes the planning question less urgent in the moment and more important over time, which is exactly the kind of question that tends to get deferred.

The better moment to examine home equity is well before a household needs it, when there is no pressure, no deadline, and the full range of options is still open. Modeled years in advance, the concentration of wealth inside the home becomes a deliberate choice rather than a default, and the household and its advisor can weigh the alternatives with clear eyes. Examined only after a liquidity need has already arrived, the same decision is made under stress, with fewer choices and less room to maneuver. Proactive planning does not promise a better outcome. It tends to produce a calmer process and a wider set of options, and for this particular segment, that is the entire point.

The bottom line

The debate over whether homeownership is a trap will continue, and the loudest voices in it will keep belonging to people deciding whether to buy. The more actionable version of the conversation, for advisors, belongs to the clients who already own, who hold a mortgage rate the market no longer offers, and whose wealth has quietly concentrated inside a home they have every reason not to touch. They are not stuck in any permanent sense. But they are a recognizable segment with a specific tension, and that tension is solvable through planning. The first step is simply to separate the home a client loves from the equity inside it, and to ask the liquidity question early enough that it can be answered on the household’s own terms.

Schedule a CHEIFS demo HERE

Disclosures

This article is for informational and marketing purposes only and does not constitute financial, tax, or legal advice. Homeowners should consult with independent, licensed financial, tax, and legal professionals for advice. CHEIFS may involve risks, fees, costs, contractual obligations, and other material considerations not appropriate for all homeowners. Homeowners and their independent advisors should carefully evaluate all available options against the homeowner’s individual financial situation, goals, and overall financial and tax strategy.

CHEIFS is a home equity investment agreement (or “HEI”), not a loan. This is not an offer or commitment. CHEIFS is subject to underwriting and approval, including property appraisal(s) and verification of credit history, property condition, title, and property insurance, among other things. Performance of the CHEIFS agreement is secured by a mortgage or trust deed, depending on the state, in no lower than second lien priority. The equity share return becomes payable upon a settlement event and is calculated as a percentage of the home’s future value, subject to the program’s cost cap. Homeowner pays an origination fee plus appraisal, title, recording fees, and other closing costs. Homeowner must occupy and maintain the property and remain current on property insurance, taxes and assessments, and payments on any other mortgages. Terms may vary and are subject to change. Additional conditions apply. Not available in all states.

Cornerstone does not offer HEI products or solicit business related to properties located in the states of NY, MN, and certain other states. Please visit cheifs.com/licensing for a list of states where CHEIFS is offered. CHEIFS is offered exclusively by Cornerstone Financing LLC, and its subsidiary Domus Funding Corp. (in California only), and does business as “Domus Funding LLC” in OH and as “Domus Funding” in NH. Principal Office: 86 Summit Ave., Ste. 201, Summit, NJ 07901. Toll-free (855) 462-4343. NMLS #2557707, www.nmlsconsumeraccess.org. CA DRE license #02248492. Not licensed in all states. Cornerstone’s HEI product is not offered under state mortgage lending licenses.

InsMark® and Wealthy and Wise+™ are service marks of InsMark LLC and are used with permission. © 2026 Cornerstone Financing LLC. “CHEIFS” is a registered service mark, and the CHEIFS logo is a service mark, of Cornerstone Financing LLC. All rights reserved.