Where the Home Equity Actually Sits

A planning read on TransUnion’s Q1 2026 Home Equity Trends Report

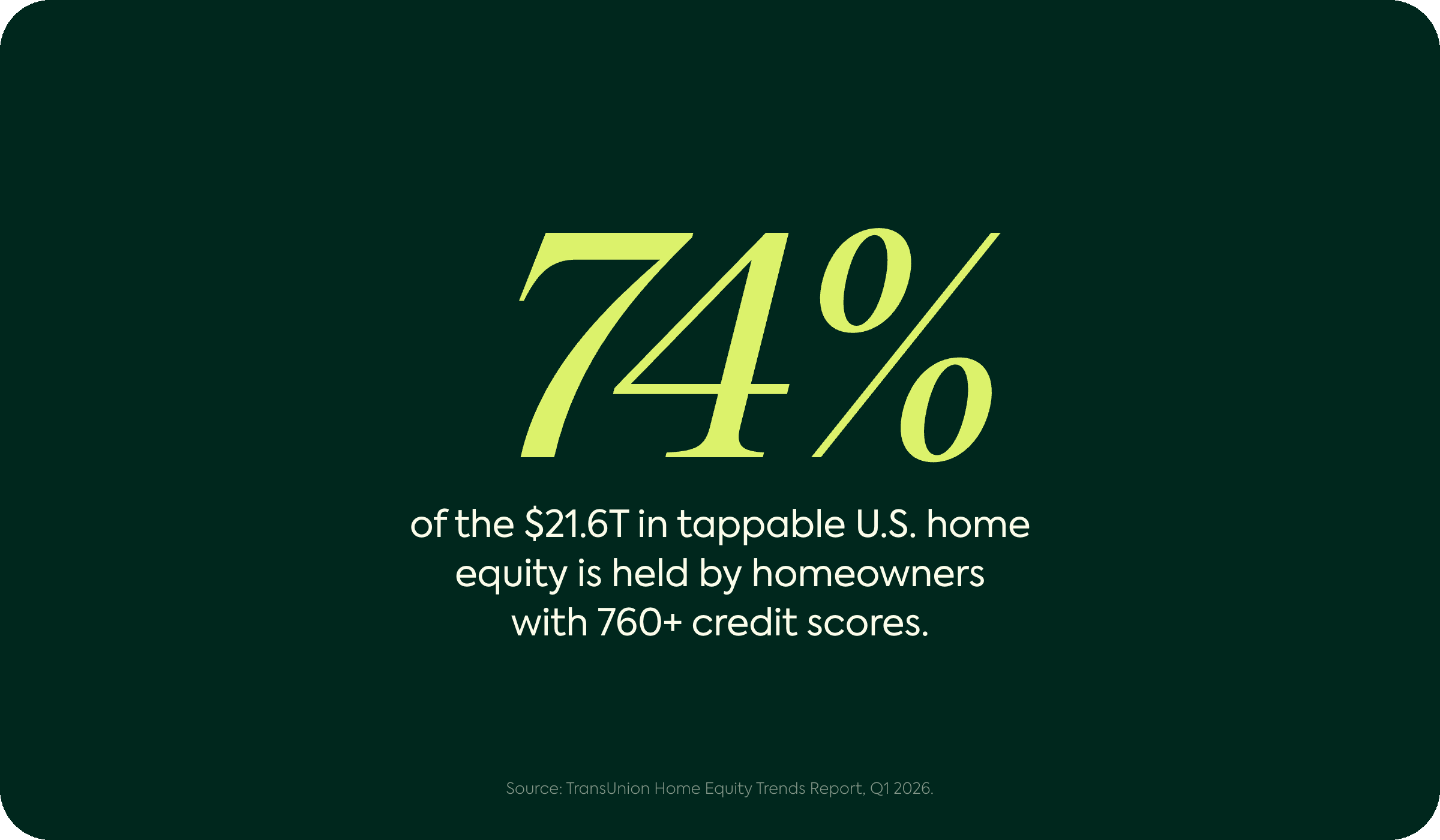

For years, the financial industry has described home equity as a single enormous number, somewhere around $35 trillion, large enough to mean everything and therefore nothing. TransUnion’s Q1 2026 Home Equity Trends Report offers a more disciplined figure, and a more useful one. Once you account only for equity that is genuinely tappable, meaning the portion of property value that remains after existing mortgage and home equity balances are deducted for creditworthy owners, TransUnion puts the number at $21.6 trillion. It is smaller than the headline we have all leaned on, and it is far more revealing, because the report also shows precisely who holds it.

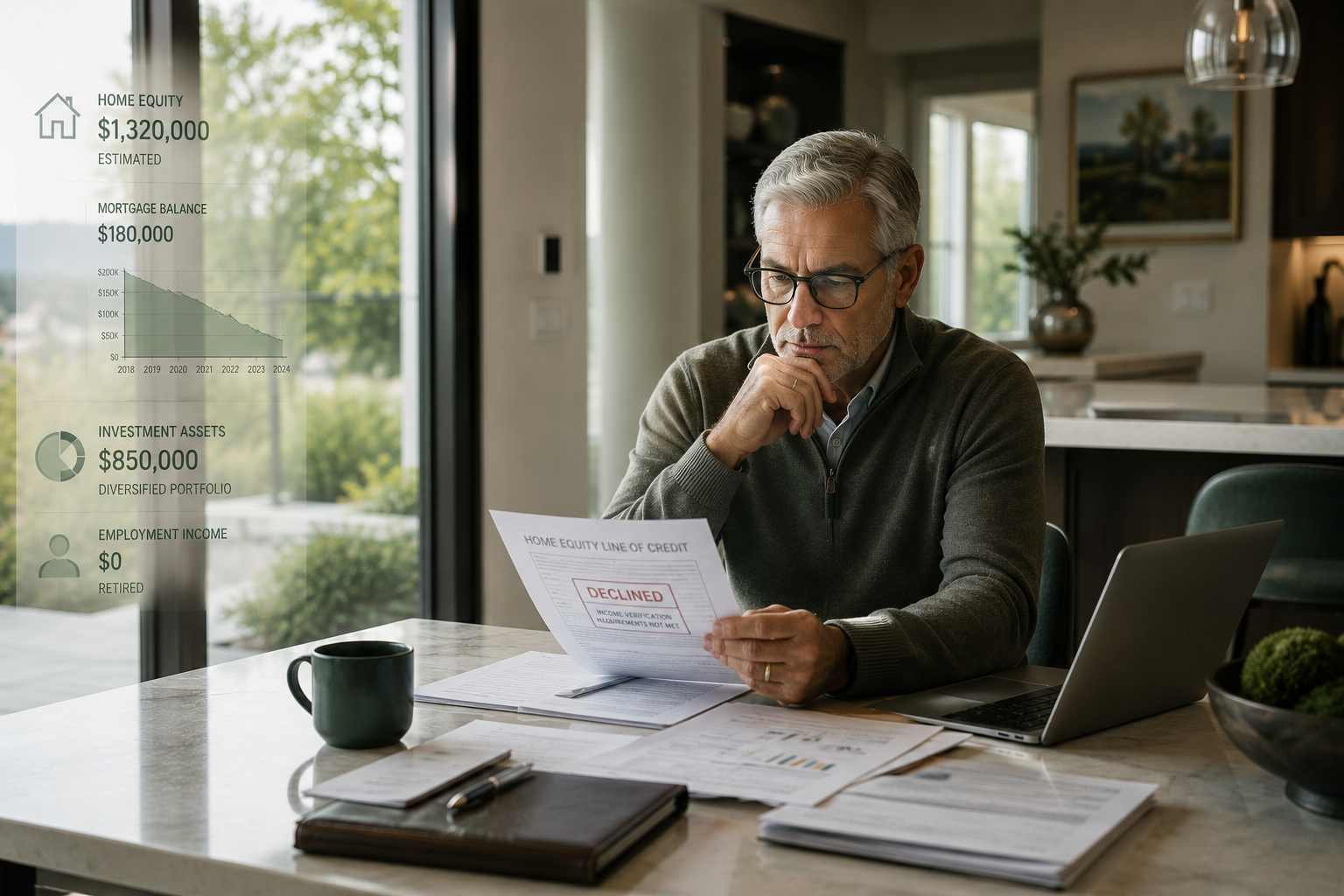

The concentration is striking. According to TransUnion, nearly three-quarters of that $21.6 trillion belongs to homeowners with credit scores above 760. These are not stretched borrowers or financially fragile households. They are among the most creditworthy owners in the country, and many of them are retired or approaching it. More than 85 million consumers hold meaningful tappable equity, with a median of roughly $277,000, and about 6.5 million hold more than a million dollars of it. The wealth, in other words, is concentrated exactly where conventional income-based underwriting tends to work least well: with people whose financial strength sits on the balance sheet rather than the pay stub.

That tension comes into sharper focus on what may be the report’s most important page. Among these high-credit owners, the average combined loan-to-value ratio is about 30 percent, with a median closer to 19 percent. Forty percent of all U.S. homes carry no mortgage at all, and roughly two-thirds of those free-and-clear owners are Baby Boomers or members of the Silent generation. Picture the household this describes. An advisor sitting across from a free-and-clear 68-year-old is not looking at a borrowing candidate. They are looking at a liquidity-planning question. The mortgage is gone, the leverage is minimal, and the relevant issue is no longer whether the client can qualify to borrow. It is how to fund the decade ahead without selling appreciated assets at an inopportune moment.

Several other findings reinforce why this matters now. Roughly half of all outstanding mortgages still carry rates below 4 percent, against a prevailing 30-year rate north of 6 percent. For a high-equity homeowner, that gap is a powerful reason to leave the existing first lien undisturbed. Refinancing into a materially higher rate to access cash is, for most of these households, a non-starter, which is part of why the pool of refinance candidates continues to shrink.

At the same time, the data shows households reaching for more expensive credit elsewhere. Average non-mortgage debt has climbed to about $8,600 per homeowner, and a meaningful share of owners now carry more than $10,000 in credit card and unsecured personal loan balances. It is a quiet disconnect worth naming. A large group of asset-rich households is taking on costlier, often variable-rate unsecured debt while sitting on record amounts of illiquid home equity that no one has put on the table.

There is a timing element as well. TransUnion estimates that roughly 415,000 home equity lines of credit will reach the end of their draw period within the next twelve months. For many of those borrowers, that transition brings payment recasts and re-qualification, often at a moment in life when income documentation has grown more complicated. Each of those is less a lending event than a planning conversation waiting to happen.

It is worth being clear about the financial health of this population, because it shapes how the conversation should be framed. Delinquency rates on both home equity lines and home equity loans remain near long-term lows, well below the levels seen in prior cycles. This is not a story about households in distress reaching for a lifeline. It is a story about financially sound owners whose largest asset happens to be the least liquid one on their balance sheet.

Put those threads together and a coherent planning picture emerges. The country’s home equity wealth is concentrated among its most creditworthy and often oldest homeowners, many of whom have little or no mortgage, every incentive to preserve a low-rate first lien, and a growing appetite for liquidity that they are currently satisfying with more expensive forms of credit. For an advisor, that is not a lending observation. It is an invitation to treat housing wealth as a planning asset alongside the portfolio, rather than as a borrowing tool of last resort.

This is the context in which some advisors are beginning to evaluate newer structures. Among them are non-recourse home equity investment agreements such as CHEIFS, which provide a homeowner with a lump sum today in exchange for a share of the home’s future value, settled at a future event such as a sale. An arrangement of this kind is not a loan. Instead of charging interest or carrying a monthly payment, the investor participates in the home’s future value when a settlement event occurs, and the homeowner takes on no new monthly payment in the meantime. Whether or not a particular household chooses to explore such a structure, the underlying planning question stands on its own. The largest underused asset on many balance sheets is the home, and the clients holding the most of it are frequently the ones least likely to be asked about it.

The TransUnion data does not prescribe a course of action, and good planning never reduces to a single product. What the numbers do is relocate the conversation. They suggest that the most meaningful home equity discussions over the next several years will not happen at the lending desk. They will happen in planning reviews, with clients who look, on paper, like they need nothing at all. A useful place to begin is a simple screen of the book: which clients are asset-rich, income-flexible, and sitting on substantial equity that has never once come up in a review?

Source: TransUnion Home Equity Trends Report, Q1 2026. Figures reflect TransUnion’s US consumer credit database.

Disclosures

This article is for financial professional use and for informational and marketing purposes only. It does not constitute financial, tax, or legal advice. Advisors should evaluate the suitability of all available options for each client’s individual situation, and homeowners should consult with independent, licensed financial, tax, and legal professionals for advice. CHEIFS may involve risks, fees, costs, contractual obligations, and other material considerations not appropriate for all homeowners. Homeowners and their independent advisors should carefully evaluate all available options against the homeowner’s individual financial situation, goals, and overall financial and tax strategy.

CHEIFS is a home equity investment agreement (or “HEI”), not a loan. This is not an offer or commitment. CHEIFS is subject to underwriting and approval, including property appraisal(s) and verification of credit history, property condition, title, and property insurance, among other things. The subject property may not be in foreclosure or bankruptcy. Performance of the CHEIFS agreement is secured by a mortgage or trust deed, depending on the state, in no lower than second lien priority. Minimum investment payment is $70,000. Owner-occupied, 1-2 unit residential properties only. The equity share return becomes payable upon a settlement event and is calculated as a percentage of the home’s future value, subject to the program’s cost cap. Homeowner pays an origination fee plus appraisal, title, recording fees, and other closing costs. Homeowner must occupy and maintain the property and remain current on property insurance, taxes and assessments, and payments on any other mortgages. Terms may vary and are subject to change. Additional conditions apply. Not available in all states.

Cornerstone acts for itself, as the investor, and not as an agent or broker for the homeowner or any third party. There is no agency relationship between Cornerstone and a homeowner related to the CHEIFS agreement.

Cornerstone does not offer HEI products or solicit business related to properties located in the states of NY, MN, and certain other states. Please visit cheifs.com/licensing for a list of states where CHEIFS is offered. CHEIFS is offered exclusively by Cornerstone Financing LLC, and its subsidiary Domus Funding Corp. (in California only), and does business as “Domus Funding LLC” in OH and as “Domus Funding” in NH. Principal Office: 86 Summit Ave., Ste. 201, Summit, NJ 07901. Toll-free (855) 462-4343. NMLS #2557707, www.nmlsconsumeraccess.org. CA DRE license #02248492. Not licensed in all states. Cornerstone’s HEI product is not offered under state mortgage lending licenses.

© 2026 Cornerstone Financing LLC. “CHEIFS CONVERTING HOME EQUITY INTO FINANCIAL SUCCESS” and “CHEIFS” are registered service marks, and the CHEIFS logo is a service mark, of Cornerstone Financing LLC. All rights reserved.