Direct Indexing’s Quiet Bottleneck: Funding the Strategy Without Triggering the Tax

Link copied

A strange thing happens at the top of a bull market: clients get richer and harder to advise at the

same time.

The last few years have manufactured concentration at scale — Nvidia’s multi-year run minted enormous embedded gains in ordinary brokerage accounts, and the private markets have done the same for a different cohort. SpaceX’s December 2025 secondary valued the company near $800 billion at about $421 a share, roughly double the $212 set just five months earlier, and a subsequent xAI merger marked it at $1.25 trillion ahead of an IPO that could rank among the largest ever. The result is a growing population of households — employees, early investors, long-term holders — sitting on outsized single-position gains.

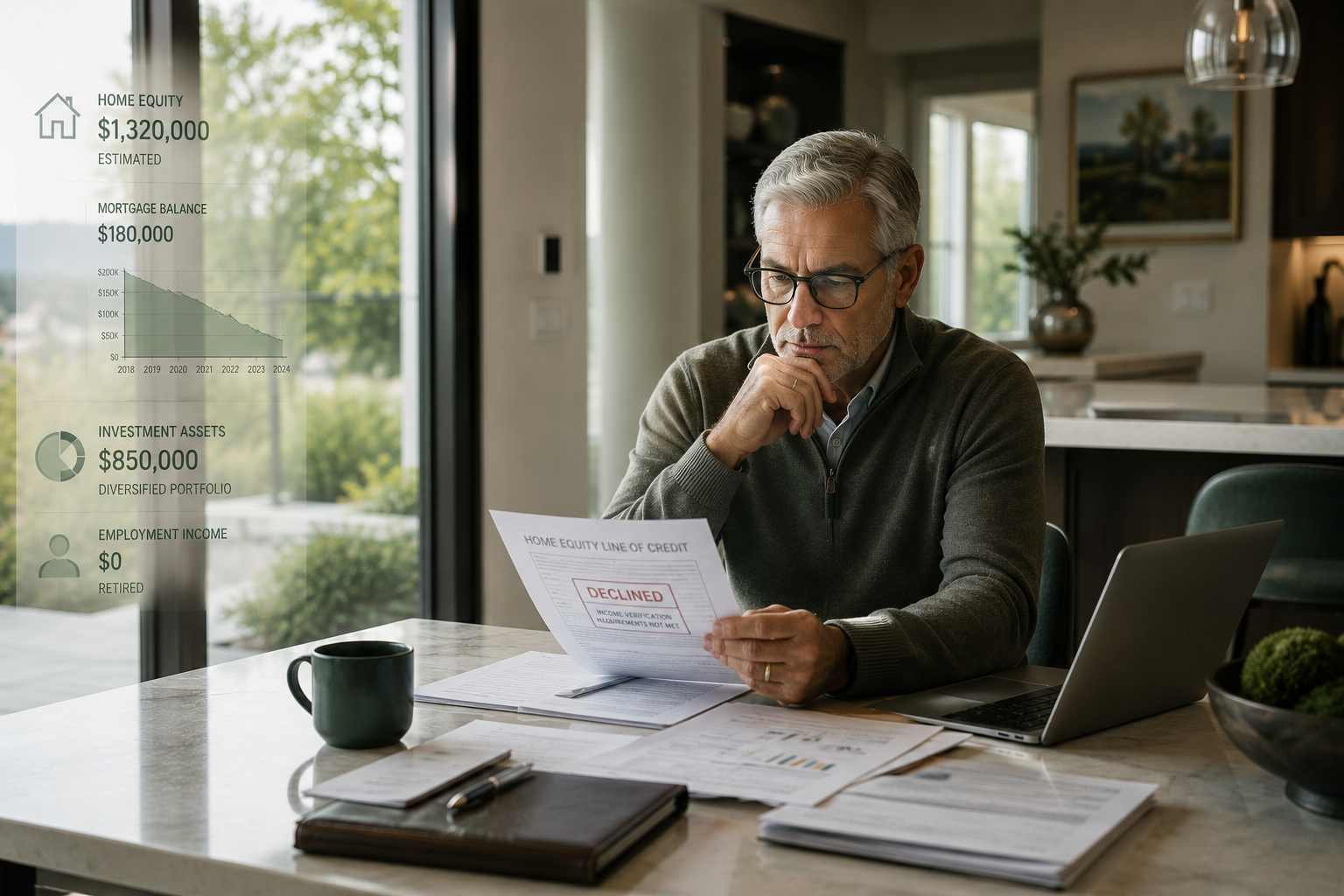

For these clients, the planning problem isn’t accumulation. It’s what comes next. A concentrated position is a risk-management issue dressed up as a success story, and the textbook answer — diversify — runs straight into a tax wall. SpaceX’s own workforce is often described as equity-rich but cash-poor, with net worth tied to a single name and liquidity available only in narrow windows. Selling to diversify realizes the gain. Not selling keeps the risk.

Why direct indexing is having its moment

This is the backdrop against which direct indexing has moved from niche to mainstream. Rather than holding an index fund, the investor owns the underlying stocks directly in a separately managed account, which lets a manager harvest losses at the individual-security level and use them to offset gains elsewhere. Cerulli projects direct indexing assets will top $800 billion by 2026, growing faster than ETFs, mutual funds, and separate accounts. For a client unwinding a concentrated position, that loss-harvesting capacity is the appeal: it can offset some of the gains realized while trimming the oversized holding over time.

Two myths are worth retiring. The first is that this is a high-minimum product. It was, briefly; it isn’t now. Fidelity offers a managed direct-indexing account at a $5,000 minimum and Altruist at $2,000 — access is no longer the gating factor. The second is that advisors have already adopted it. They haven’t. Cerulli found only 14% of advisors are aware of direct indexing and actively recommend it, and a separate survey put the share who feel familiar or very familiar with how it works at just 34%. The strategy is scaling faster than the advisor base understands it — which is precisely where a planning conversation creates value.

The bottleneck no one budgets for

Here is the part that gets lost in the product literature: a tax-aware strategy still has to be funded, and how it’s funded can quietly undo the point of it.

The instinct is to fund the new account by selling existing positions. But for a client whose gains are concentrated in the very holdings they’d sell, that realizes the tax bill the strategy was designed to manage — a self-defeating loop. Analysts who model this directly reach the same conclusion: liquidating a highly appreciated portfolio to move into a direct index can offset the long-term benefit, and funding with cash from income or a liquidity event is the better path when deferral options are gone.

That reframes the question advisors actually face. It isn’t which strategy — it’s what capital funds it, and every source carries an opportunity cost:

- Sell appreciated assets to raise cash, and you trigger gains and disrupt the allocation.

- Withdraw from the portfolio, and you interrupt the compounding the plan depends on.

- Draw down cash reserves, and you weaken the liquidity earmarked for everything else.

None of these is wrong. But each spends something the plan was counting on, which is why some advisors widen the lens to the rest of the client’s balance sheet.

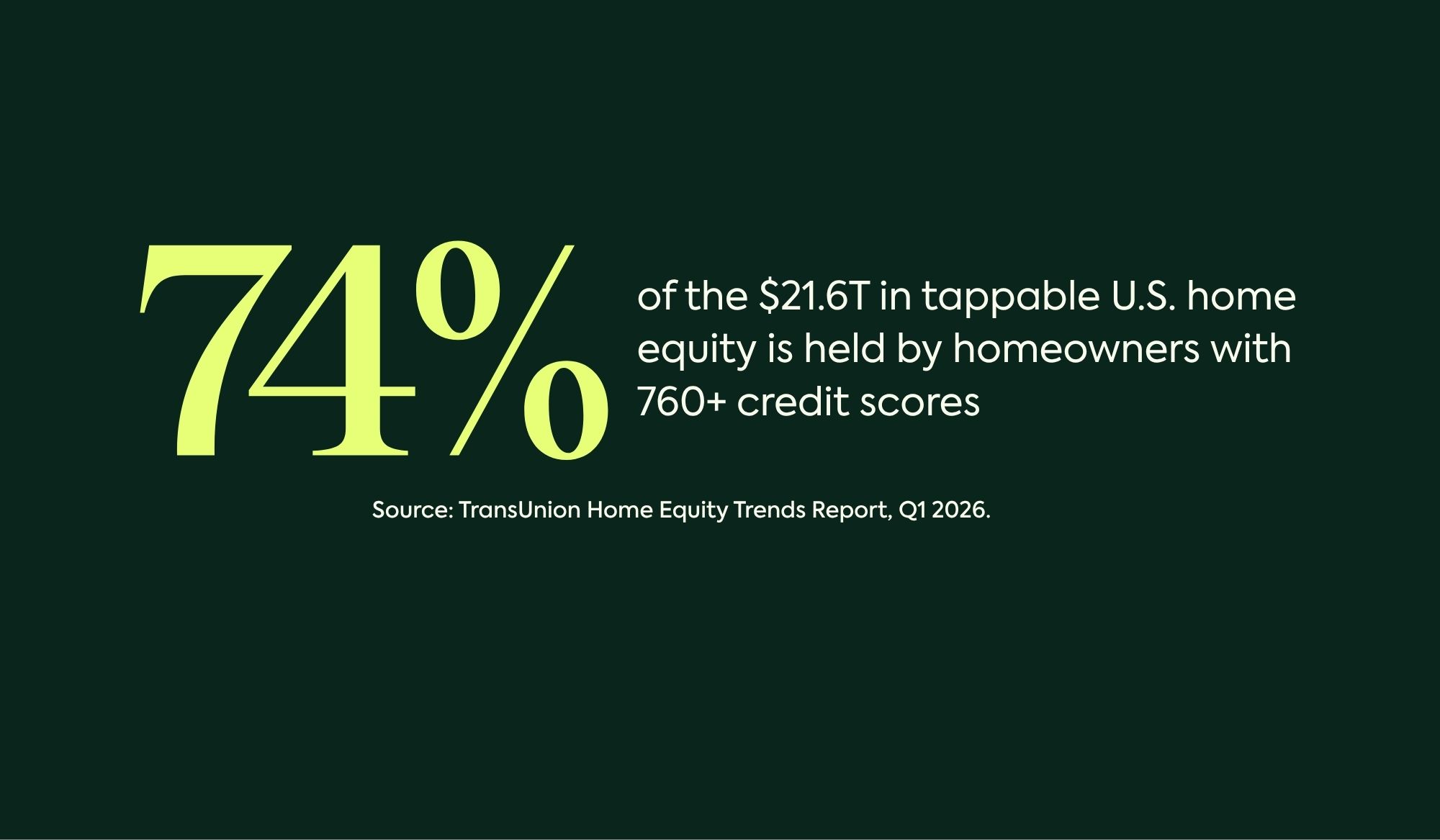

Home equity as a planning input

For homeowners, the largest underused asset on that balance sheet is usually the house. It rarely enters the funding conversation, partly because the traditional tools — refinancing, a HELOC — add monthly payments and interest at exactly the wrong moment in a client’s life. Newer structures change that calculus, which is why some advisors now evaluate home equity alongside the portfolio when sizing a liquidity need.

CHEIFS®, offered by Cornerstone Financing, is one example of a modern home equity investment agreement (HEI): a non-recourse arrangement that provides homeowners proceeds today in exchange for a share of the home’s future value, with no monthly payments and the homeowner retaining ownership and occupancy. Settlement occurs at a later event — a sale, a permanent move-out, or the homeowner’s passing — rather than on a fixed schedule. Like any financing structure, it carries costs, obligations, and risks that in some situations may outweigh the benefits, and suitability depends entirely on the client’s circumstances and the guidance of their tax and financial advisors.

The point isn’t that home equity is the answer. It’s that the funding source is a planning decision in its own right — one that can either preserve the invested capital a strategy is meant to grow, or quietly erode it. As concentrated gains pile up and tax-aware investing goes mainstream, the advisors who think carefully about where the money comes from will be a step ahead of those focused only on where it goes.

Sources

Cerulli Associates — direct indexing to top $800B by 2026 — https://www.cerulli.com/press-releases/cerulli-associates-projects-direct-indexing-assets-to-top-800-billion-by-2026-while-outpacing-growth-of-etfs-mutual-funds-and-smas

Broadridge — direct indexing minimums ($5K Fidelity, $2K Altruist) — https://www.broadridge.com/next/articles/etfs-make-room

Russell Investments — direct indexing and concentrated positions — https://russellinvestments.com/us/blog/direct-indexing-resource-center

Cache — funding direct indexing without liquidating appreciated assets — https://usecache.com/companion/direct-indexing-in-2025-basics-tradeoffs-and-comparisons

Fortune — SpaceX $800B secondary, 2026 IPO — https://fortune.com/2025/12/13/spacex-ipo-plan-2026-secondary-offering-insider-share-sale-800-billion-valuation/

KeepTrack — SpaceX $1.25T xAI merger and ownership — https://keeptrack.space/deep-dive/who-owns-spacex

Augustus Wealth — SpaceX employee concentration and liquidity — https://augustuswealth.com/blog/what-know-about-space-x-valuation/